Global Construction Equipment Market Overview (2026-2034)

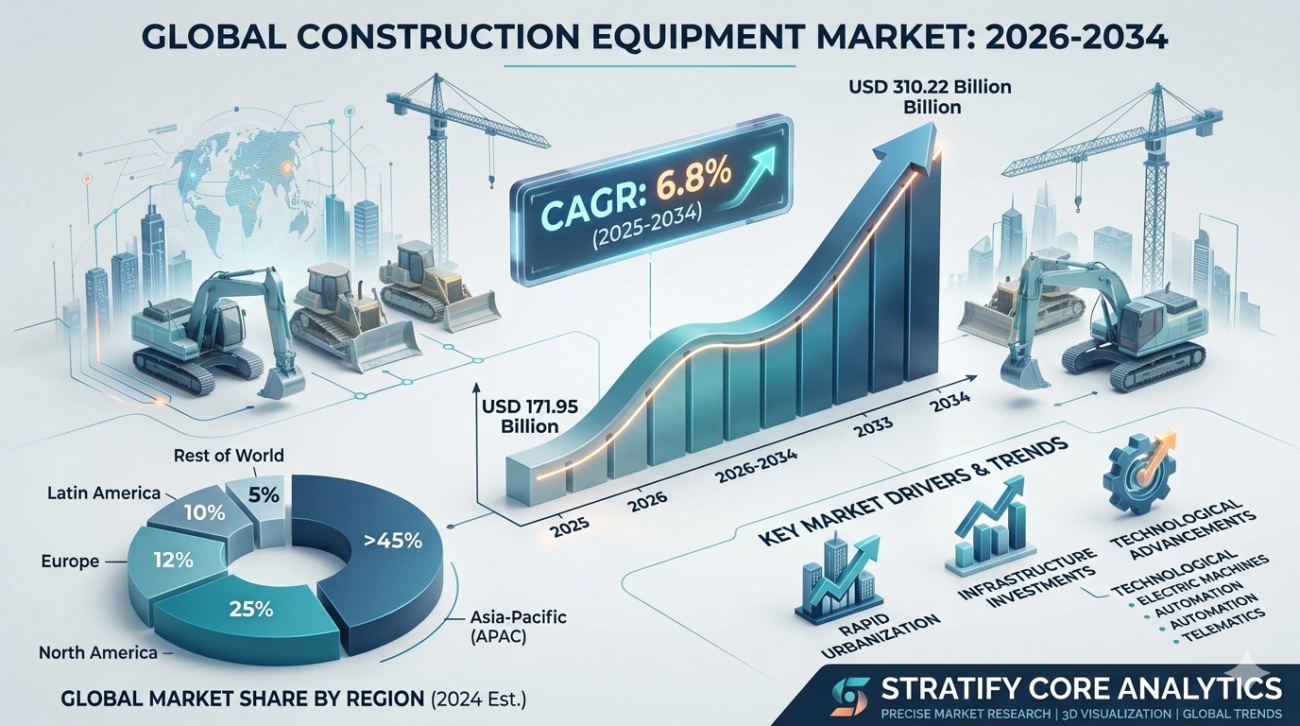

The global construction equipment market was valued at USD 171.95 billion in 2025 and is anticipated to grow to USD 310.22 billion by 2034, exhibiting a compound annual growth rate of 6.8%.

The global construction equipment market stands as one of the most strategically significant segments within the broader industrial machinery and heavy equipment industry. Driven by rapid urbanisation, unprecedented infrastructure investments, and the continued expansion of residential, commercial, and industrial construction activities worldwide, the market has evolved into a multi-billion-dollar ecosystem that plays a central role in shaping the built environment across every continent.

Construction equipment are a lot of machines that people use when they are building things. This includes machines like excavators and bulldozers and motor graders that help move earth around. There are also machines like cranes and hoists and forklifts that help people lift and move things. Construction equipment also includes machines that help make concrete and fix roads. Then there are machines that help lift things up and get surfaces ready. Each type of construction equipment is important in its way, and people need different types of construction equipment in different parts of the world and for different kinds of projects. Construction equipment is really important for construction, and people use all kinds of construction equipment to get the job done.

The Asia-Pacific region is still a part of the global construction equipment market. It has more than 45 percent of the total market. This is because of countries like China and India and Japan and Southeast Asia. These places are doing a lot of construction work like building cities and roads and power plants and factories. China is the construction market in the world. So it needs a lot of construction equipment. The Asia-Pacific region is really important for the construction equipment market. China is a part of this market.

North America and Europe have market shares. This is because they are upgrading their infrastructure. They also have public-private projects. People want construction machines that save energy and work with computers. Latin America is growing steadily. This is because of housing projects, road construction and industrial development. Countries like Brazil, Mexico and Colombia are getting foreign investment. This is good for equipment manufacturers.

The construction equipment market is changing fast. Old machines are being improved with technologies. Machines are becoming electric and automatic. This will make construction more productive and sustainable.

Key Construction Equipment Market Trends

The construction equipment industry is really changing the way things are done. The construction equipment industry is going through a change because of new technology, people wanting to be more sustainable and customers wanting different things. It is very important for the people who make this equipment, the people who sell it the people who invest in it and the people who make the rules to understand what is happening in the market so they can make decisions.

One of the trends in the construction equipment market is that more and more people are using electric and hybrid machines. Because the rules about the environment are getting stricter and more people want to be kind to the earth, the companies that make this equipment are making battery-electric and hydrogen-powered machines instead of the old diesel-powered ones. Companies like Volvo CE, Caterpillar and Komatsu are already making excavators and loaders, which shows that they are changing the way they make things. The construction equipment market is really moving towards hybrid machines.

Automation and robotics are also changing the construction equipment market. People are using machines that can be controlled from afar and machines that can do things on their own to make construction sites safer and more precise. Some companies are even making machines that can do everything by themselves using intelligence and machine learning. This is not an idea for the future; it is something that is happening now. The construction equipment market is getting more automated.

The construction equipment market is also using something called ‘telematics and IoT technologies’. This means that machines have sensors and can connect to the internet to send information about how they’re working, how much fuel they are using and where they are. This helps construction companies make sure their machines are working well, do not break down much and cost less to own. The construction equipment market is getting more connected.

Some construction equipment is being made to be smaller and more flexible, which is good for building things in cities where space is limited. People really want mini-excavators, loaders and small cranes, especially in big cities in Asia, Europe and North America. The construction equipment market is moving towards compact equipment.

More and more people are renting construction equipment of buying it which is changing the way things are done. This is because contractors want to spend money and be able to use different machines when they need to. This has made a market for renting equipment and companies that help people rent machines. The construction equipment rental market is growing.

Something called Building Information Modeling (BIM) is also changing the way people use and buy construction equipment. When people use BIM to plan their construction projects they can choose the machines and make sure they are used in the best way. The construction equipment market is using BIM more and more.

Key Construction Equipment Market Restraints

The global construction equipment market is growing fast, but it also faces a lot of challenges that can slow it down. One big problem is that construction equipment is very expensive to buy. This equipment, like excavators and cranes, costs a lot of money, which is hard for small construction companies to afford.

This makes it tough for the market to grow in developing countries and among construction companies who may not have access to good financing options. Another issue is that the prices of materials like steel and aluminium keep changing. This affects the cost of making construction equipment. Can impact the price of the equipment and the profitability of the companies that make it.

We also have to think about problems with the supply chain, which were an issue during the COVID-19 pandemic. There is a shortage of semiconductors and electronic parts which are needed for modern construction equipment. This has caused delays in production and delivery of equipment for some manufacturers. The fact that we rely on places for these critical parts is a big risk.

The construction equipment market and the construction industry also face a shortage of workers. New construction equipment is very advanced. Requires special skills to operate. In places there is a big gap between the skills that workers have and the skills they need, which limits how well new equipment can be used and reduces productivity.

There are also rules about the environment and emissions which can be a challenge for companies that make construction equipment. These companies have to spend a lot of money to meet these rules, which can increase the cost of equipment for smaller companies.

Sometimes infrastructure projects are. Cancelled because of political issues, budget problems or regulatory hurdles. This can reduce the demand for construction equipment in areas. Projects in developing countries are especially prone to problems, like financing challenges and economic uncertainty. Finally, it can be hard for people to buy construction equipment in some places, especially where the financial system is not well developed. High interest rate financing options and currency risks make it even tougher to buy equipment in some developing countries, which limits the growth of the construction equipment market.

Construction Equipment Market Key Opportunities

The global construction equipment market presents a rich landscape of growth opportunities that stakeholders across the value chain can strategically capitalize on over the coming decade.

The global push toward green and sustainable infrastructure represents one of the most compelling opportunities in the construction equipment market. Governments worldwide are channelling substantial public investment into renewable energy infrastructure – including solar farms, wind energy installations, and hydropower projects – all of which require specialized construction machinery. This transition creates substantial demand for equipment that is not only capable of handling large-scale energy infrastructure projects but also meets the sustainability benchmarks set by project developers and financiers.

The electrification of construction equipment is an immense market opportunity for manufacturers willing to invest early and decisively in zero-emission machinery. With many countries committing to construction site emission restrictions in urban areas in the coming years, early movers in electric equipment will have a significant competitive advantage. Battery technology advancements, declining costs of energy storage systems, and improving charging infrastructure are making electric construction machinery increasingly viable across a broader range of machine categories.

Emerging economies across Africa, South Asia, Southeast Asia, and Latin America represent substantial untapped growth opportunities. These regions are experiencing rapid population growth, urban migration, and expanding middle classes that are driving unprecedented demand for housing, transportation infrastructure, and commercial real estate. As these economies formalize and develop their construction industries, demand for construction equipment – both new and refurbished – is set to surge.

The rapid advancement of construction technology, including autonomous and remotely operated equipment, creates opportunities for manufacturers to differentiate through technology leadership. Companies that can successfully integrate AI, machine learning, and computer vision into their equipment can offer customers significant productivity and safety advantages, commanding premium pricing and building stronger customer loyalty.

The growing equipment rental market represents a significant business model opportunity. As contractors increasingly prefer flexible, asset-light approaches to equipment access, there are opportunities for traditional manufacturers to expand into equipment-as-a-service (EaaS) models, digital rental platforms, and fleet management solutions. This creates recurring revenue streams and deeper customer relationships beyond the initial equipment sale.

Refurbishment and remanufacturing of used construction equipment is an underutilised but rapidly growing opportunity. As sustainability awareness increases and end-users seek cost-effective alternatives to new equipment, there is growing demand for certified remanufactured machines that offer comparable performance at a lower price point. This segment also aligns with circular economy principles increasingly embedded in public procurement frameworks worldwide.

Finally, digitalization across construction project management creates opportunities for equipment manufacturers to bundle intelligent software solutions with their hardware. Integrated telematics platforms, predictive maintenance services, and digital fleet management tools offer manufacturers new avenues to generate service revenue while adding measurable value to customers through improved machine availability, reduced operating costs, and enhanced project productivity.

Construction Equipment Market Key Drivers

The global construction equipment market is growing fast but it also faces a lot of challenges that can slow it down. One big problem is that construction equipment is very expensive to buy at. This equipment, like excavators and cranes costs a lot of money which’s hard for small construction companies to afford. This makes it tough for the market to grow in developing countries and among construction companies who may not have access to good financing options.

Another issue is that the prices of materials like steel and aluminum keep changing. This affects the cost of making construction equipment. Can impact the price of the equipment and the profitability of the companies that make it. We also have to think about problems with the supply chain, which were an issue during the COVID-19 pandemic. There is a shortage of semiconductors and electronic parts which are needed for modern construction equipment. This has caused delays in production and delivery of equipment for some manufacturers. The fact that we rely on places for these critical parts is a big risk.

The construction equipment market and the construction industry also face a shortage of workers. New construction equipment is very advanced. Requires special skills to operate. In places there is a big gap between the skills that workers have and the skills they need which limits how well new equipment can be used and reduces productivity. There are also rules about the environment and emissions which can be a challenge for companies that make construction equipment. These companies have to spend a lot of money to meet these rules, which can increase the cost of equipment for smaller companies.

Sometimes infrastructure projects are. Cancelled because of political issues, budget problems or regulatory hurdles. This can reduce the demand for construction equipment in areas. Projects in developing countries are especially prone to problems, like financing challenges and economic uncertainty. Finally, it can be hard for people to buy construction equipment in some places especially where the financial system is not well developed. High interest rate financing options and currency risks make it even tougher to buy equipment in some developing countries, which limits the growth of the construction equipment market.

Construction Equipment Market Segment Insights

The global construction equipment market is segmented across multiple dimensions including equipment type, application, end-user industry, power source, and distribution channel. Understanding these segments and their growth dynamics is essential for stakeholders seeking to identify high-value investment and business development opportunities.

By equipment type, earthmoving equipment commands the largest share of the market, accounting for approximately 40 percent of global construction equipment revenue. Excavators represent the dominant machine category within this segment, given their versatility across a wide range of applications including digging, trenching, material loading, and demolition. Bulldozers, motor graders, backhoe loaders, and skid-steer loaders are also major contributors to this segment, each finding particular demand in roadway construction, mining, and land development applications.

Concrete equipment forms the second-largest segment by equipment type and includes concrete mixers, batching plants, concrete pumps, and transit mixers. The urbanization boom in Asia and the Middle East has been particularly supportive of this segment, as high volumes of ready-mix concrete are required for residential towers, commercial developments, and infrastructure projects. The growing adoption of ready-mix concrete over site-mixed concrete is further driving demand for transit mixers and concrete pumping equipment.

Cranes and lifting equipment represent a critical segment within the construction equipment market, with tower cranes, mobile cranes, and crawler cranes all experiencing steady demand growth driven by high-rise construction, industrial plant construction, and wind energy installation projects. The offshore and marine construction sector adds additional demand for heavy lift crane equipment, particularly in regions with active offshore energy development.

Road construction equipment – encompassing asphalt pavers, compactors, milling machines, and road rollers – is experiencing robust growth aligned with global road network expansion and road maintenance programs. Governments across developing regions are prioritizing road connectivity as a foundational element of economic development, creating sustained demand for road construction machinery in markets such as India, Sub-Saharan Africa, and Southeast Asia.

By power source, diesel-powered equipment continues to dominate the market due to its established performance characteristics and extensive global servicing infrastructure. However, the electric and hybrid segment is growing at a significantly faster pace, supported by regulatory pressures, technological maturation, and total cost of ownership advantages in certain operational scenarios, particularly for compact machinery and equipment used in indoor or emission-restricted environments.

By end-user, the residential construction sector represents the largest market segment globally, followed closely by infrastructure, commercial construction, and industrial construction. The relative weight of these segments varies significantly by region, with infrastructure construction dominating in developing Asia and Africa, while commercial real estate and industrial construction are larger contributors in North America and Europe.

By distribution channel, direct sales from manufacturers to large contractors remain the primary channel for heavy equipment, while dealers and distributors play a critical role in reaching medium and small-sized construction companies. The digital and online procurement channel is growing, particularly for equipment rentals and spare parts, as construction companies increasingly adopt digital procurement tools and platforms to streamline their purchasing operations.

Construction Equipment Market, Regional Analysis

The global construction equipment market exhibits distinct regional characteristics shaped by local economic conditions, infrastructure maturity, government policies, and construction activity levels.

Asia-Pacific leads the global market with the largest revenue share, driven by the construction superpowers of China, India, Japan, and South Korea. China’s Belt and Road Initiative, domestic urbanization, and industrial development projects have sustained extremely high equipment utilization rates. India’s National Infrastructure Pipeline, valued at over USD 1.4 trillion, is one of the most ambitious infrastructure programs globally and is generating transformative demand for construction equipment across road, rail, port, airport, and urban infrastructure segments.

North America, led by the United States, is a mature but actively growing market. The Infrastructure Investment and Jobs Act, combined with private sector construction activity in industrial, logistics, and data center development, is sustaining strong equipment demand. The U.S. market is also at the forefront of adopting advanced telematics and autonomous machinery, setting standards that will influence global market evolution.

Europe’s construction equipment market is characterized by high regulatory sophistication, with stringent Stage V emission standards driving innovation in engine technology and electrification. Key growth areas include Germany, France, the UK, and the Scandinavian countries, where sustainable construction practices and urban regeneration projects are prominent. The EU’s Green Deal and Next Generation EU fund are also channeling investment into clean energy infrastructure with significant construction equipment requirements.

The Middle East is experiencing an equipment demand surge linked to landmark development programs in Saudi Arabia, the UAE, Qatar, and Kuwait. Saudi Arabia’s Vision 2030 megaprojects, including NEOM – the planned smart city – and the Red Sea tourism development, are among the most ambitious construction programs globally. Qatar’s post-FIFA World Cup infrastructure legacy continues to support construction activity, while Kuwait and Bahrain are pursuing significant urban expansion programs.

Africa presents a long-term high-growth opportunity for construction equipment. The continent’s rapidly expanding population, urbanization rate, and infrastructure deficit create compelling demand for construction machinery across road, housing, energy, and water infrastructure. Sub-Saharan Africa, in particular, is attracting increasing infrastructure investment from multilateral development banks and bilateral partners, including China’s BRI funding.

Latin America’s construction equipment market is dominated by Brazil, Mexico, and Colombia. Brazil’s infrastructure concession programs and housing development initiatives are driving equipment procurement, while Mexico benefits from near-shoring-driven industrial construction investment and government road and energy programs. Colombia’s expanding road network and urbanization programs also contribute to regional growth.

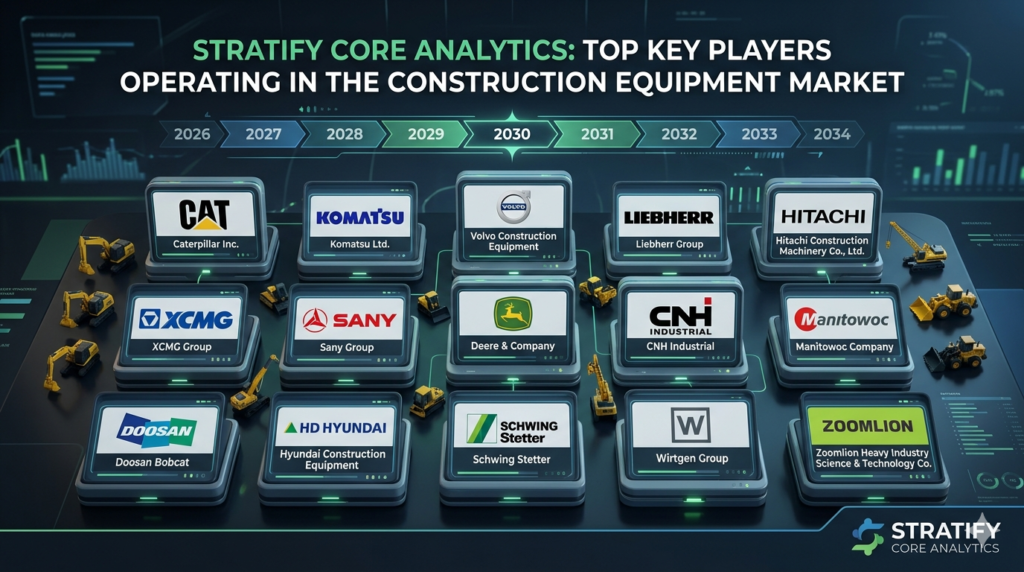

Top Key Players Operating in the Construction Equipment Market

The global construction equipment market is served by a diverse mix of multinational corporations and regional leaders. Below are the top key players driving innovation, market share, and global supply:

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment

- Liebherr Group

- Hitachi Construction Machinery Co., Ltd.

- XCMG Group

- Sany Group

- Deere & Company

- CNH Industrial

- Manitowoc Company

- Terex Corporation

- Doosan Bobcat

- HD Hyundai Construction Equipment

- Schwing Stetter

- Wirtgen Group

- Zoomlion Heavy Industry Science & Technology Co.

FAQ – Construction Equipment Market

-

What is the current size of the global construction equipment market?

The global construction equipment market was valued at approximately USD 180 billion in 2024 and is projected to grow at a CAGR of around 5 to 6 percent through 2032, reaching an estimated market value in excess of USD 270 to 290 billion by the end of the forecast period. Growth is primarily driven by large-scale infrastructure investment programs, rapid urbanization across emerging economies, and increasing adoption of technologically advanced and sustainable construction machinery across all major global markets.

-

Which region dominates the global construction equipment market?

Asia-Pacific is the dominant region in the global construction equipment market, accounting for more than 45 percent of total global market revenue. China and India are the primary contributors to this regional dominance, driven by massive government-led infrastructure programs, urban development initiatives, and high levels of private construction investment. Countries such as Indonesia, Vietnam, and Bangladesh are also contributing to regional growth as their economies expand and construction activity accelerates. Asia-Pacific is expected to maintain its lead throughout the forecast period, supported by ongoing megaproject pipelines and sustained urbanization trends.

-

What are the key growth drivers of the construction equipment market?

The key growth drivers of the construction equipment market include rapid global urbanization, large-scale government infrastructure investment programs, growing residential and commercial construction demand, technological advancement in machinery including electrification and automation, and expanding activity in the energy and mining sectors. Additionally, public-private partnerships (PPPs) as a project delivery model are increasing the pipeline of construction projects globally. The shift toward sustainable infrastructure, coupled with digitalization of construction operations through telematics and AI-powered fleet management solutions, is also driving higher equipment utilization and procurement rates.

-

How is the electrification trend impacting the construction equipment market?

The electrification of construction equipment is one of the most transformative trends currently reshaping the industry. In response to tightening environmental regulations and carbon neutrality commitments, leading manufacturers including Volvo CE, Caterpillar, Komatsu, and XCMG are rapidly expanding their portfolios of battery-electric and hybrid machines. Electric compact equipment such as mini-excavators, compact loaders, and telehandlers are already commercially available, and development of larger electric machines is progressing rapidly. While challenges around battery range, payload limitations, and charging infrastructure remain, the total cost of ownership advantages and regulatory tailwinds are accelerating adoption, making electrification a defining theme in the construction equipment market for the next decade.