Automotive Sensor Fusion Market Overview

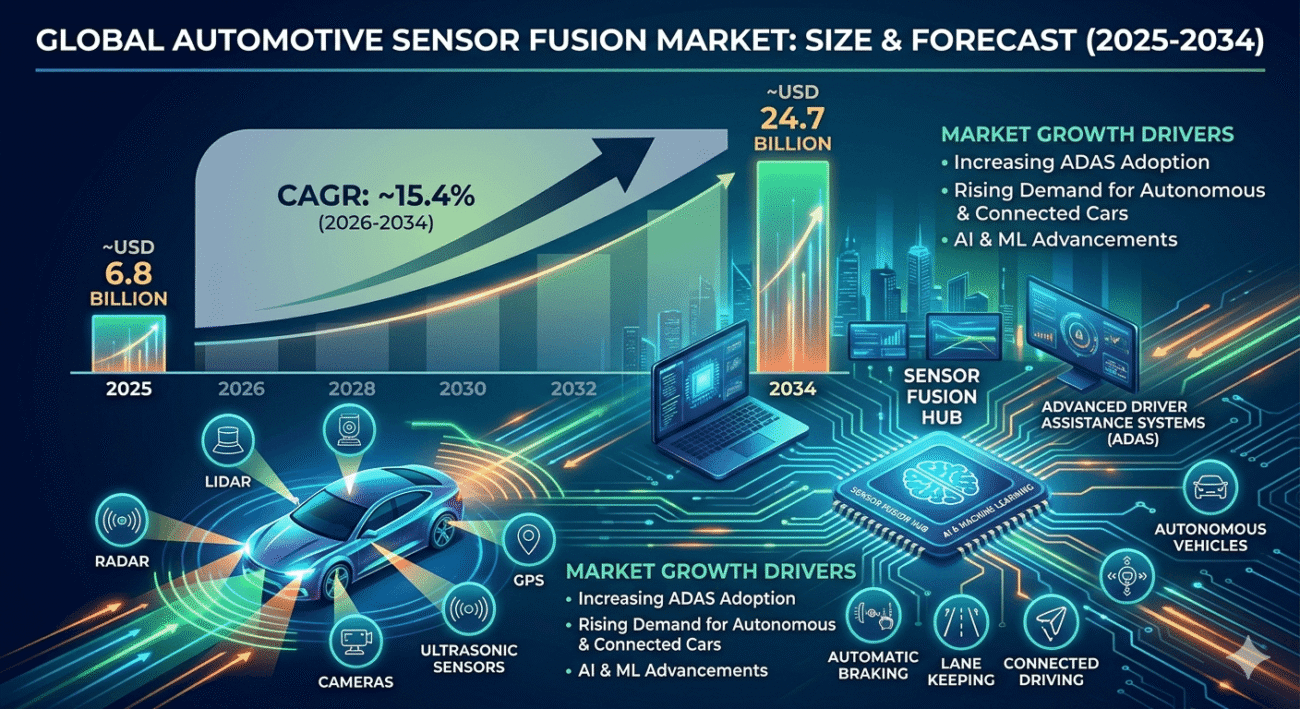

The global automotive sensor fusion market was Valued At $ 6.8 billion in 2025 And Is Expected To Reach $ 24.7 billion in 2034. The Automotive sensor fusion market is expected to grow at a robust CAGR of 15.4% from 2026 To 2034. The global automotive sensor fusion market is on a growth trend, owing to the increasing implementation of ADAS, AV, and connected car applications.

Sensor fusion technology integrates the output of various types of sensors, such as radar, LIDAR, cameras, ultrasonic, GPS to obtain accurate environmental perception for improved vehicle safety and performance. Automotive sensor fusion systems use data collected from multiple sensors to help vehicles make intelligent decisions in terms of driving, enhancing the driver’s situation awareness, and driving autonomous cars. The global market share of automotive sensor fusion is expected to grow significantly in the next few years.

Increasing vehicle safety awareness and accident Prevention is another factor driving Theglobalautomotivessensor fusion marketis Thegrowing emphasis on thesafetyandprevention of road accidents is driving theautomotivessensor fusion market. The global market is responding to the stringent automotive safety regulations imposed by authorities and increasing the consumers’ desire for vehicles that support preventing accidents using vehicle intelligence, such as the blind-spot monitoring system, Automatic Emergency Braking(AEB), adaptive cruise control system (ACC), Parking assist system, lane departure warning system (LDW). The function of the sensor fusion is to provide unparalleled levels of reliability for these safety features.

Development in self-driven and assisted-driving cars- Another factor that contributed to the growth in global automotive sensor fusion is an increment in a number of self-driving and semi-autonomous vehicles.Automotive vehicles that can interpret and react in real-time to surroundings, identify obstacles, and track the surrounding flow of vehicles use sensors fusionsystem.The global market has a tremendous opportunity for Automotive OEs and technology providers to develop sensor fusion algorithms and AI-based perception systems that optimize performance and safety for self-driving vehicles.

Growing demand for connected automotive technology- Many of the modern vehicles are equipped with a communication system to execute V2V and V2I communication, and the growth of connected automotive is continually rising, which can be leveraged to develop new intelligent transportation systems, including intelligent traffic management and parking assist systems through extensive Data acquisition, management and fusion from a variety of sensors. The rising adoption of electric vehicles (EVs) is pushing the global market for automotive sensor fusion to grow.

Newer models of Electric Vehicles (EVs) come equipped with a significant amount of advanced digital systems and intelligent safety features, owing to their hardware infrastructure that is naturally receptive to integration with the latest technology, including sensors and AI-based vehicular systems. As the market for electric vehicles (EVs) increases, the demand for sophisticated sensor fusion systems will also grow. In the Automotive sector,AI, Machine Learning (ML), and Edge Computing are having a positive influence on the Automotive sensor fusion market by enabling them to efficiently collect and analyze data from various sensors, increasing the vehicular perception and responsiveness times.

Machine Learning (ML) algorithms improve vehicle autonomous capabilities and adaptability to a variety of environments. Different sensor fusion Technologies- Camera sensors play a pivotal role in Automotive sensor Fusion systems because they provide highly detailed image output and high resolution. Radarsensors are crucial for the autonomous vehicle application as they detect the obstacle, the speed of approach of the obstacle, and the distance between the vehicle and the obstacles. LiDAR technology has become prevalent because of its 3D map generation capabilities and it creates an unparalleled view of the world surrounding the vehicle.

Fusing all the various types of technologies for automotive sensor fusion enhances the reception acuity of the vehicular system. Region’s outlook in the global automotive sensor fusion market- North America and Europe dominate the global automotive sensor fusion market due to their well-established automotive industries, stringent safety regulations, and wide adoption of automated driving technology.

Asia-Pacific is a rapidly growing region because of the rising vehicle production volume, prevalence of EV technology, and demand for smart transport systems. Competitive landscape of the global automotive sensor fusion market – The automotive sensor fusion market is highly fragmented and is characterized by fierce competition among global market stakeholders, technology developers, and semiconductor suppliers.

Research and development invested by the key market players, which focus on optimizing sensor accuracy, decreasing system costs, increasing the real-time speed of the processing units of automotive sensor fusion systems, coupled with strategic alliances between major automotive OEs and cutting-edge AI companies, is expected to drive automotive towards the future of fully automated vehicles.

Despite robust future projections, the automotive sensor fusion market is facing certain challenges, such as high costs of installation, the possibility of cyber threats, and complexities associated with the development of the autonomous driving system. However, increasing consumer demand for intelligent vehicular features and sophisticated vehicular safety systems, along with a significant rise in the utilization of AI-based automotive talent systems, will maintain and push the future market growth in the long term.

Key Automotive Sensor Fusion Market Trends

Many of the driving trends that are currently happening within the sector of autonomous vehicles, AI and automobile safety have driven this recent boom. Currently, the most significant driving trend is the growth of advanced driver assistance systems (ADAS) in both personal and commercial vehicles, most notably lane holding assist, automatic braking, adaptive cruise control, and blind spot assist, and their impact on the increased demand for sensor fusion systems. Currently gaining considerable momentum in the automotive sensor market is how autonomous vehicles rely on cameras, LiDAR, GPS, radar, and ultrasonic sensors to obtain a precise representation of the automobile’s surrounding environmental model so the vehicles can drive safely.

The machine learning and artificial intelligence market segment for automotive sensor fusion solutions is expanding. These models are excellent for analyzing tremendous quantities of disparate and intricate data streams simultaneously in order to achieve greater accuracy in collision avoidance, and also learning optimal vehicle response. High-resolution three-dimensional mapping data obtained from LiDAR systems is proving indispensable for autonomous navigation of vehicles as prices continue to plummet from the previous year’s high price points.

Additionally, the automotive sector demand for on-board computational processes using edge computing in sensor fusion devices is very prominent. The most pressing objective for many in the automotive sensor fusion industry, whether it’s in LiDAR systems, ultrasonics, or the range radar and other cameras, is to create a vehicle “perceptive,” meaning to give vehicles a more all-encompassing awareness. The exponential adoption of electric and smart vehicles into the automotive sensor market comes as no surprise. As automobile manufacturers move toward autonomous vehicle capabilities with smart connectivity features, the utilization of in-depth, well-integrated sensor fusion technology will steadily grow, particularly since automobile manufacturers are heavily invested in automating the self-driving aspects. Vehicles that communicate with other vehicles and external systems are a huge trending concern for many in the auto industry, otherwise called Vehicle to Everything, or V2X. Sensor fusion systems are being applied to such systems that communicate across the vehicle as well as with traffic systems and even with pedestrians.

As this trend in vehicle communication proliferates into the auto industry, the increased interest in the systems needed for connectivity will grow. As complex data-based driving systems are further relied upon to run and operate automobiles, this aspect of cybersecurity will continue to be a hot issue that continues to increase for car and automotive manufacturers to secure vehicle communication networks, automobile software, and sensor output data from various intrusions and hacking attacks.

The high-performance silicon vendors that focus on auto chips is the expanding sector of advanced processors to support these high-functioning sensor fusion and automobile autonomous driving systems. Such processor-backed AI chip sets will allow cars to process and assimilate an increasingly greater amount of data and other driving inputs required to support these increasingly demanding autonomous driving applications. Strategic alliances between numerous component makers, including those providing LiDAR systems, as well as radar components and ultrasonic sensors, and a few camera lens suppliers and machine vision integrators are burgeoning, underscoring the overall strategic importance of partnerships to speed up development.

Key Automotive Sensor Fusion Market Key Restraints

Despite significant technological advancements and growing adoption of autonomous driving systems, the automotive sensor fusion market faces several restraints that may limit its growth during the forecast period. One of the primary challenges is the high cost associated with sensor fusion systems and advanced automotive sensors. Technologies such as LiDAR, radar, high-resolution cameras, and AI-powered processors require substantial investment, increasing overall vehicle production costs.

The complexity of integrating multiple sensors into a unified system represents another major restraint. Automotive sensor fusion requires precise synchronization and calibration between various sensor technologies to ensure accurate environmental perception. Any inconsistency or malfunction within the system can affect vehicle safety and operational reliability, making integration highly challenging for manufacturers.

Cybersecurity risks are becoming increasingly significant as vehicles become more connected and software-driven. Sensor fusion systems process large amounts of real-time data and communicate with external networks through connected vehicle technologies. This connectivity creates vulnerabilities that can expose vehicles to cyberattacks, data breaches, and unauthorized access, raising concerns among manufacturers and consumers.

The lack of standardized regulations and technical frameworks for autonomous driving systems also poses challenges for market growth. Different countries and regulatory authorities have varying safety standards and testing requirements for autonomous vehicles and ADAS technologies. The absence of global standardization can slow product development and increase compliance complexities for automotive manufacturers.

Environmental factors can negatively impact sensor performance and system reliability. Adverse weather conditions such as heavy rain, fog, snow, dust, and poor lighting can affect the accuracy of cameras, radar systems, and LiDAR sensors. Sensor limitations in challenging driving conditions may reduce the effectiveness of autonomous driving and advanced safety systems.

The shortage of skilled professionals specializing in artificial intelligence, machine learning, automotive software engineering, and sensor technologies is another significant restraint. Developing and maintaining advanced sensor fusion systems requires highly specialized expertise, and the growing demand for skilled talent is creating workforce challenges across the automotive technology sector.

High research and development costs continue to impact the market, particularly for smaller automotive companies and startups. Developing advanced sensor fusion algorithms, AI-powered perception systems, and autonomous driving platforms requires substantial investment in software development, testing, validation, and semiconductor technologies.

Data processing and computing power requirements also present operational challenges. Automotive sensor fusion systems generate enormous volumes of data from multiple sensors simultaneously. Processing this data in real time requires high-performance computing systems and advanced automotive processors, increasing energy consumption and hardware complexity.

Consumer concerns regarding autonomous vehicle safety and reliability may slow adoption of sensor fusion technologies. Many consumers remain hesitant to fully trust autonomous driving systems due to fears related to software failures, sensor inaccuracies, and accident risks. Public acceptance of autonomous mobility solutions will play a crucial role in market expansion.

Supply chain disruptions and semiconductor shortages have significantly affected the automotive industry in recent years. Sensor fusion systems rely heavily on advanced semiconductor chips and electronic components. Shortages of critical components can delay vehicle production, increase manufacturing costs, and impact market growth.

Another restraint is the limited affordability of advanced sensor fusion technologies in low-cost vehicle segments. While premium and luxury vehicles increasingly incorporate sophisticated ADAS and autonomous features, budget-friendly vehicle categories may face slower adoption because of cost sensitivity and pricing pressures.

Lastly, legal and liability concerns associated with autonomous driving technologies continue to create uncertainty within the market. Determining responsibility in the event of accidents involving autonomous or semi-autonomous vehicles remains a complex issue. Regulatory challenges and legal uncertainties may affect the pace of commercialization and adoption of advanced sensor fusion systems in the automotive industry.

Automotive Sensor Fusion Market Key Opportunities

The global Automotive Sensor Fusion Market is witnessing significant growth opportunities due to rapid advancements in autonomous driving technologies, increasing vehicle safety regulations, and the growing integration of connected mobility solutions. One of the most promising opportunities in the market is the rising adoption of advanced driver assistance systems (ADAS). Governments and automotive safety organizations worldwide are mandating the inclusion of safety features such as automatic emergency braking, lane departure warning, adaptive cruise control, and blind-spot monitoring systems. These technologies rely heavily on sensor fusion platforms, creating substantial growth opportunities for automotive manufacturers and technology providers.

The expansion of autonomous and semi-autonomous vehicle development presents another major opportunity for the automotive sensor fusion industry. Autonomous vehicles require precise environmental perception capabilities achieved through the integration of cameras, radar, LiDAR, ultrasonic sensors, and GPS systems. Sensor fusion technologies enable these vehicles to process real-time data accurately and make intelligent driving decisions, making them a critical component of next-generation mobility systems.

The increasing adoption of electric vehicles is also generating strong opportunities for sensor fusion technologies. Electric vehicles are often equipped with advanced digital architectures and intelligent mobility systems that require sophisticated sensor integration. As EV manufacturers continue investing in autonomous driving capabilities and smart connectivity features, demand for advanced sensor fusion systems is expected to rise significantly.

Artificial intelligence and machine learning integration offer substantial growth opportunities within the market. AI-powered sensor fusion systems improve object recognition, road condition analysis, and decision-making capabilities in autonomous vehicles. Machine learning algorithms enable continuous improvement of driving performance by analyzing traffic patterns, environmental conditions, and driver behavior in real time.

The rapid development of smart cities and intelligent transportation systems is another important market opportunity. Governments are investing heavily in connected infrastructure, traffic management systems, and vehicle-to-everything (V2X) communication technologies. Automotive sensor fusion systems play a crucial role in enabling communication between vehicles, traffic signals, pedestrians, and infrastructure networks, supporting safer and more efficient transportation systems.

The growing demand for premium and luxury vehicles equipped with advanced safety features is contributing to market expansion. Consumers increasingly prefer vehicles offering enhanced driver assistance technologies, automated parking systems, collision avoidance features, and intelligent navigation solutions. Luxury automotive manufacturers are integrating high-performance sensor fusion platforms to differentiate their products and improve user experience.

Advancements in LiDAR technology are creating new opportunities within the market. LiDAR sensors provide highly accurate 3D environmental mapping and object detection capabilities essential for autonomous driving systems. Continuous innovation and declining production costs are making LiDAR technology more commercially viable for mass-market vehicle applications.

The emergence of edge computing and high-performance automotive processors is further expanding market potential. Edge computing enables real-time data processing directly within vehicles, reducing latency and improving response times. Advanced semiconductor technologies are allowing automotive sensor fusion systems to process complex sensor data more efficiently, supporting the development of fully autonomous driving platforms.

Commercial vehicle automation is another growing opportunity for the automotive sensor fusion market. Logistics companies, public transportation operators, and fleet management providers are increasingly investing in autonomous trucks, delivery vehicles, and smart transportation systems. Sensor fusion technologies help improve operational efficiency, reduce accidents, and optimize fleet management operations.

Emerging economies across Asia-Pacific, Latin America, and the Middle East are also offering significant growth opportunities. Rising vehicle production, increasing urbanization, expanding road infrastructure, and growing adoption of advanced automotive technologies are supporting market expansion in these regions. Government initiatives promoting road safety and intelligent transportation systems are expected to further accelerate sensor fusion adoption globally.

Automotive Sensor Fusion Market Key Drivers

Key Market Drivers: Increased demand for ADAS and autonomous driving technologies in vehicles: Rising concerns about road safety and traffic accidents have pushed governments and automakers to implement intelligent vehicle safety solutions. This is driving the demand for sensor fusion to improve vehicle perception and enable proper decision-making.

Safety regulations enacted by government: Several governing bodies in countries like North America, the Middle East and Africa, Asia Pacific and Europe mandate auto manufacturers to integrate safety features in commercial as well as passenger vehicles such as automatic emergency braking systems, automatic collision avoidance and lane assistance systems.

This enhances the sale of sensor fusion technology across all vehicle segments, to allow better understanding and interpretation of road scenarios. Rapid rise in autonomous and semi-autonomous cars: In the development of autonomous and semi-autonomous cars, seamless integration of sensors like LiDAR, radar and cameras is essential, enabling a car to understand road surroundings and avoid collisions and obstacles. To overcome this challenge, advanced and sophisticated sensor fusion technology has enabled easy merging of the collected information.

Rise of electric vehicles (EVs): EVs are usually equipped with advanced digital systems that integrate with new connected car and IoT devices, for the functioning of all automotive components. Moreover, the increasing emphasis by auto manufacturers to increase AV integration for the enhancement of EVs necessitates adequate functioning of several types of sensors, which will be taken care of by an automobile sensor fusion system. Advanced technologies like AI, machine learning, edge computing: Technologies such as AI, ML, Edge Computing, etc., are making automobiles smarter and also helping with faster data processing for vehicle systems.

Auto manufacturers are leveraging AI and ML solutions in order to interpret the vast amount of data processed from different vehicle sensors and use this data for better-decision making. Emergence of connected and smart mobility solutions: The global automotive industry is adapting to mobility solutions which include in-vehicle communication systems and external communications through connected vehicle platforms V2V & V2I systems to assist in better understanding of road conditions and to avoid potential road accidents, hence it’s creating good demand of this technology across global auto markets. Growing demand for luxury and premium vehicles: This sector is usually ahead when it comes to adopting innovative technologies for better functionality and superior consumer experience.

The luxury vehicle segment of the market, with safety and driver assistance features that integrate well with a sensor fusion platform, is gaining traction, fuelling demand in this market segment. Increase in R&D activities by manufacturers: Auto makers are rapidly investing in R&D for improving AV and ADAS technology, creating a significant amount of opportunities for sensor and software vendors. For instance, collaboration of car manufacturers with tech providers like NVIDIA Corporation and Intel, in order to advance the overall system functionality and capabilities in automated vehicles.

Expansion of smart transportation infrastructure and intelligent transport systems: Governments worldwide are keenly interested in Smart City Initiatives and these initiatives involve the deployment of infrastructure for intelligent transport solutions. Such infrastructure is used to enable communication between vehicles and traffic management systems; hence, automobile sensor fusion plays a major role. Advancement of Semiconductor Technology: Advanced automotive sensors need efficient automotive microchips that offer rapid real-time data processing; the latest semiconductors are making it possible to facilitate the smooth implementation of such sensors in vehicles.

Better computing power and efficiency can help in creating reliable and robust automotive sensing and processing solutions in real time. Public awareness about road accidents and vehicle safety: With rising cases of road accidents and increased focus on vehicle safety features by consumers, automakers are focusing on integrating robust automotive sensor fusion technologies in their vehicle ranges to enhance passenger safety and support a safer driving experience.

Automotive Sensor Fusion Market Segment Insights

Automotive sensor fusion is very diverse and fragmented in several areas such as sensor types, vehicle types, technology types, applications types and propulsion types. All these segments can contribute, with varying intensity, to the growth of the automotive sensor fusion market as whole. The global automotive sensor fusion market has been segmented, by sensor type, into: Radar sensors, LiDAR sensors, Camera sensors, Ultrasonic sensors, and other sensors.

The Radar sensor segment held the highest market share in the automotive sensor fusion market, as radar sensors can be used for detecting the presence of objects, measuring the velocity of vehicles and are less affected by any of the environmental conditions. Radar sensor types is widely useful in many advanced driver assistance systems, such as adaptive cruise control, collision avoidance systems, and blind-spot detection systems. Camera sensors can produce high-resolution images which can be further used for identifying objects and lanes present in the path of the vehicle, identifying traffic signs and for driver monitoring systems, thus resulting in a significant share in the automotive sensor fusion market.

The LIDAR sensor segment is poised to emerge as the fastest-growing segment, owing to the sensor’s ability to generate three-dimensional environment models and identify objects with remarkable precision, which are necessary for the navigation and perception system of truly autonomous vehicles. Autonomous vehicle manufacturers increasingly are integrating LiDAR sensors in vehicles because they facilitate comprehensive environment mapping and object recognition, which helps in making appropriate driving decisions.

Ultrasonic sensors are mainly utilized in proximity or close-range distance detection applications, such as parking assist and close proximity collision avoidance, and provide high accuracy and reliability when measuring closeness. The global automotive sensor fusion market has been segmented by vehicle type into passenger vehicles and commercial vehicles.

The passenger vehicles segment generated a leading share in the global automotive sensor fusion market owing to the growing awareness of connected, intelligent and autonomous mobility and the increasing consumers’ desire for advanced in-car features for their vehicles. The luxury segment and the premium vehicle segment adoption have shown faster acceptance to advanced sensor fusion techniques. Commercial vehicles have recently witnessed increased adoption of sensor fusion technology with a focus on augmenting advanced vehicle safety features, including collision avoidance and autonomous capabilities, among other safety and efficiency gains. These vehicles hold a robust demand among fleet operators and logistics businesses.

The global automotive sensor fusion market has been segmented by technology type into hardware and software.The hardware comprises components such as the various sensors, processor, and communication devices, electronic control units (ECUs), etc., while the software portion comprises various data fusion platforms, artificial intelligence-based perception engines, machine learning algorithms, and decision-making algorithms. By application type, the global automotive sensor fusion market has been segmented into: adaptive cruise control, lane departure warning systems, blind-spot detection, autonomous emergency braking (AEB), parking assist, traffic sign recognition (TSR), driver monitoring system (DMS) and others.AEB and adaptive cruise control segments acquired a substantial share of the automotive sensor fusion market, as governments have implemented strict regulations mandating these systems and a substantial percentage of the general consumers are now actively seeking such safety features in their vehicles.

The autonomous vehicle segment is expected to witness the fastest growth during the stipulated forecast period, owing to the significant penetration of AV technology in the vehicle technology stack requiring robust and efficient sensor fusion systems. The automotive sensor fusion market has been analyzed based on propulsion type and divided into: internal combustion engine (ICE) vehicles, hybrid electric vehicles (HEV), and electric vehicles (EV). The EV and hybrid vehicle technologies, which were fundamentally designed to incorporate a high degree of digitisation, will continue to lead in terms of the adoption rate for sophisticated sensor fusion techniques.

Automotive Sensor Fusion Market, Regional Analysis

Strong regional market dynamics are fueling the automotive sensor fusion market

The article assessed strong regional growth dynamics of the global automotive sensor fusion market owing to the growth in automotive manufacturing capacity, government safety regulations, technology advancements, and investments into the autonomous mobility ecosystem in different major regions like North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa region.North America to represent a sizable share of the automotive sensor fusion market

The North American region is to represent a sizable market share in the automotive sensor fusion market, driven by the accelerating pace of development of autonomous technologies, increasing R&D investments in the automotive sector, and the presence of leading global technology players. Robust and growing investments into the autonomous-driven vehicles, AI-enabled mobility solutions, and advanced safety systems by the U.S. Automotive manufacturing industry (which is considered one of the world’s largest automotive sectors) have made a tremendous contribution towards the automotive sensor fusion market of the region. With rising adoption rates, auto-ADAS features are rapidly adopted in the North American region, both by commercial vehicles and private automobiles, due to regulatory safety standards adopted by the U.S. National Highway Traffic Safety Administration and Transport Canada encouraging auto manufacturers to integrate a fully operational suite of auto-autonomous systems in their advanced vehicles, along with increasing customer interests and rising demand.

European countries to foster the innovation growth in the automotive sensor fusion market

Auto-ADAS demand has been considered as one of the primary factors driving growth in the European auto sensor fusion market due to the implementation of various regulations by European countries pertaining to vehicle safety standards. The automotive manufacturers and solution providers in Europe are investing in research and development of various research and developmental aspects of the automotive AI mobility, auto-autonomous driving platform, sophisticated smart transport infrastructure etc. With various countries like Germany, the UK, Sweden and France pushing innovations towards autonomous technologies, they are also fostering the adoption of these advanced solutions across the region. The trend towards growing urbanization, steady vehicle sales, and the growing demand for safer and cleaner modes of transportation significantly impacts vehicle manufacturing, with increased attention on tech-advanced vehicles due to changing customer preferences.

Rapid growth in the Asia-Pacific automotive sensor fusion market is expected over the forecast period

Asia-Pacific is expected to grow with the fastest rate in the automotive sensor fusion market during the forecast period. Increasing vehicle sales, growing pace of urbanization and quick implementation of smart cities, along with rapid pace of adoption of advanced technologies by the nations across the Asia-Pacific region, are all set to drive and shape the global automotive sector with the adoption of advanced vehicles and autonomous solutions.

China is estimated to account for the largest share in the automotive sensor fusion market due to the substantial investments by China towards the development of autonomous systems along with the wider integration of intelligent transportation systems, smart cities and huge production capacity for green vehicles. It is expected that growing investments in R&D, along with the presence of global tech companies and a well-established infrastructure, are likely to boost its market growth in the automotive sensor fusion market going forward in the region.

Moderate increase in the Latin American automotive sensor fusion market

The increasing vehicle sales driven by consumer interest, along with the growing auto manufacturing industry, are major drivers for the auto sensor fusion market of the Latin American region. Both the Brazilian and Mexican auto industries contribute heavily towards increasing automotive sales of the Latin American region and the increasing adoption rate of vehicle technology driven by changing consumer preferences is a key factor towards the growth of the auto sensor fusion market. With growing investments towards automotive mobility driven by the rise in urbanization and the economic growth across the Latin American region, vehicle manufacturing is seen increasing, which gives rise to increased market opportunities for various international firms to capitalize.

Rising investments in automotive mobility across the Middle East and Africa region

Middle East and Africa witnessed a moderate increase in the automotive sensor fusion market over the past few years. While the Middle East & Africa region is gradually growing in terms of smart cities and technological advancements, aiming for efficient transit systems. Major GCC countries are accelerating the adoption of new technologies and modern strategies to drive innovation and build smart cities infrastructure and are also investing to meet evolving automotive requirements of various vehicle types like light and heavy vehicles, that may or may not be integrated with an appropriate autonomous technology as expected.

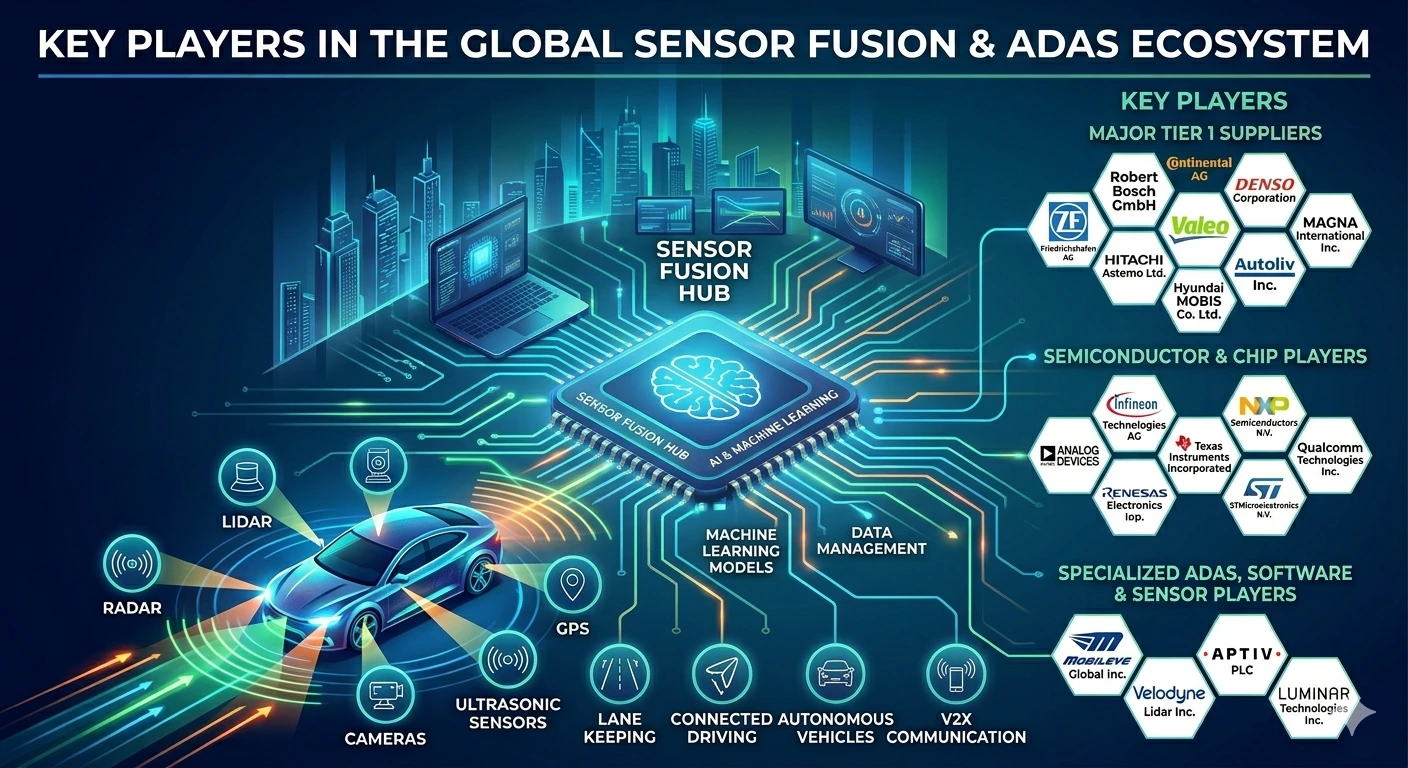

Top Key Players Operating in the Automotive Sensor Fusion Market

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Valeo SA

- Aptiv PLC

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Magna International Inc.

- Autoliv Inc.

- Mobileye Global Inc.

- Velodyne Lidar Inc.

- Luminar Technologies Inc.

- Qualcomm Technologies Inc.

- Renesas Electronics Corporation

- Hitachi Astemo Ltd.

- Hyundai Mobis Co. Ltd.

- STMicroelectronics N.V

FAQ

What is automotive sensor fusion?

Automotive sensor fusion is a technology that combines data from multiple sensors such as cameras, radar, LiDAR and ultrasonic sensors to improve vehicle perception, safety and autonomous driving performance. Automotive sensor fusion makes cars safer and smarter by combining data from different sensors.

Why is sensor fusion important in autonomous vehicles?

Sensor fusion is important in vehicles because it improves the reliability and accuracy of autonomous driving systems by integrating multiple sensor inputs and reducing the limitations of individual sensors. Sensor fusion makes autonomous vehicles safer and more efficient.

Which sensors are commonly used in sensor fusion systems?

Common sensors used in automotive sensor fusion systems include radar sensors, LiDAR systems, cameras, ultrasonic sensors, GPS modules and inertial measurement units. These sensors help make cars safer and more efficient.

Which region dominates the automotive sensor fusion >

Asia-Pacific currently dominates the automotive sensor fusion market because of strong automotive manufacturing capabilities, increasing electric vehicle adoption and government investments in autonomous mobility technologies. The automotive sensor fusion market in Asia-Pacific is driven by the demand for more efficient vehicles.