Global Application Processor Market Overview

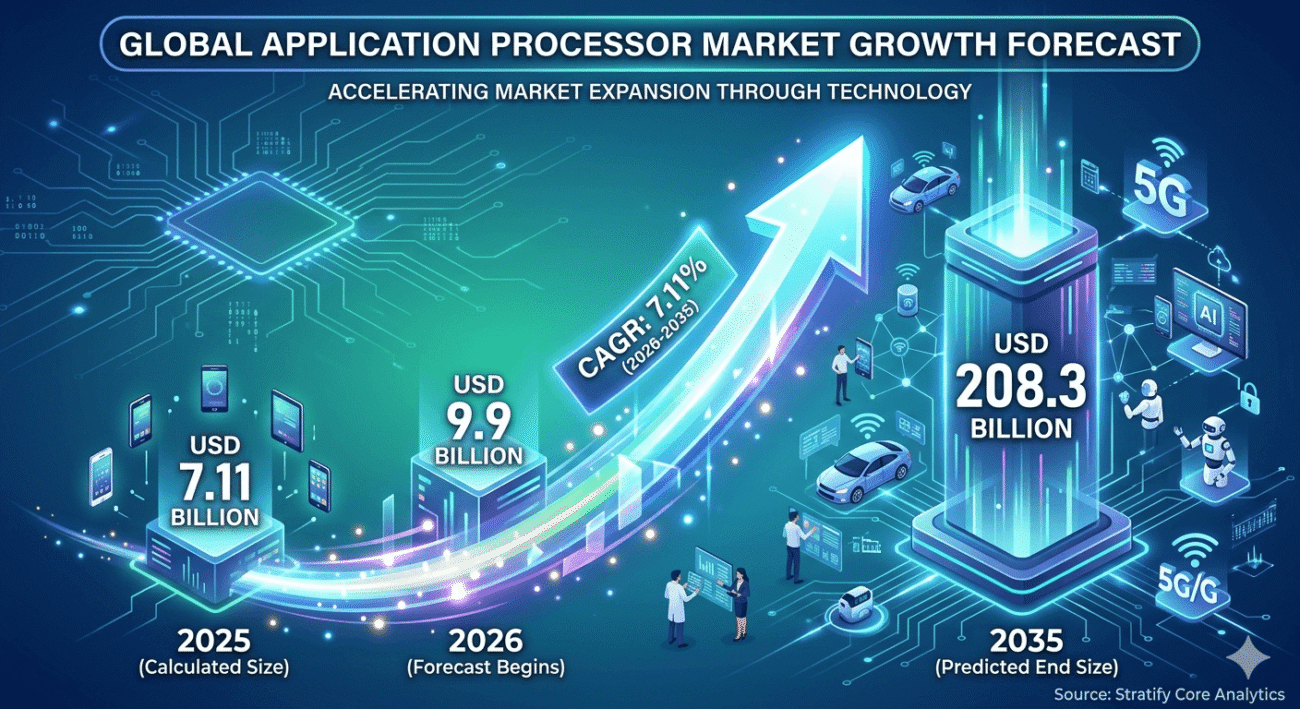

Application Processor Market size is reached 7.11 billion USD in 2025 and it was projected to rise from 9.9 billion USD in 2026 and 208.3 billion USD in 2035 at a CAGR of 7.11% during the forecast period.

The application processor market is a major section within the advanced electronics and semiconductor industry. Application processors, in particular are a type of integrated circuit that is designed for complex operating systems and application specific functions used in consumer gadgets such as smartphones, tablet computers, laptops, in-car information & communication module, portable computers, games and IoT gadgets. Application processors are an essential type of computer cores that drive media, AI operations, graphics, communications and various compute-intensive features in all modern consumer electronics and communication gadgets.

Rising demand for high end application processors is driven by rapid growth of intelligent consumer devices in both developed and emerging countries. Manufacturers of mobile smartphones are continuously upgrading chipsets in smartphones to promote superior camera, AI functionality, 5G supported features, augmented reality, and gaming. The demand for higher clock rates, lower power consumption, less heat dissipation and excellent graphics have also prompted chip manufacturers to focus on R&D in developing latest Application processors for different applications.

The transformation that took place in mobile computing is revolutionizing the competition between the semiconductor suppliers in the application processor market. Key players operating in this industry are rigorously competing to produce efficient nanometer architecture capable of higher transistor density and better power consumption, for a specific processing speed. The development of 3nm and 5nm wafers helped the silicon manufacturers in making processors that are armed with dedicated AI based learning cores and performance cores to handle intensive workloads without impacting the battery performance of portable devices.

In addition to this, the integration of edge computing and AI in portable devices is helping the growth of the market. Recent applications in consumer gadgets are being enabled with dedicated subsystems for neural network based learning and edge based intelligence. These enabled AI accelerators help the real time performance acceleration of the perception and detection of objects, speech, and natural interactive modes in the device. This new integration of features has greatly improved the user experience for smartphones, driver-less cars, and factory based automation.

The fastest growing end-user segment of the Application processor market is the automotive industry. Modern vehicles require powerful computer systems to perform all electro-mechanical operations of advanced driver assist systems, self-driving capability of vehicles, digital instrument clusters and Satellite navigation systems. Application processors are necessary to provide the processing power required for navigation, vehicle-to-vehicle connectivity, data fusion and real-time infographic visualization on these complex and sophisticated in car systems. The transition from conventional car to electrically powered vehicle (EPV) and driver-less car technology is expected to boost the demand for advanced automotive-based application processor hardware considerably.

Use of Application processor is observed in Cloud and Edge computing platforms. Cloud based data and services are supported by local processing units designed for rapid data computation by either third party tool or Application processors. The implementation of edge enabled applications and industrial imaging is putting heavy demands on low-latency and lower power consumption to be implemented effectively.

Geographically, the application processor market is dominated by the Asia-Pacific regions due to large scale production facility of silicon chips, consumer gadget production units and rising consumption base for smart devices in China, South Korea, Taiwan and India. The North America application processor market accounts for highest market shares globally due to presence of leading semiconductor design companies and hi-tech gadget manufacturers, and development center of advanced software solutions. The European market also witnessed steady growth for application processors mainly due to expanding automotive electronics and industrial automation sector.

The application processor market comprises numerous key stakeholders, including chip designers or Fabless companies, silicon manufacturers, Integrated Device Manufacturers (IDMs), software development companies and Original Equipment Manufacturers (OEMs). Increasing partnerships between these stakeholders are focused on enhancing and boost product innovation in the market and increasing coordination between hardware and software capabilities. The semiconductor suppliers are aggressively competing in the global application processor market with improved computing speed, AI functionality, subsystem design, graphics capability and power saving capabilities to capture the major share in the market.

- Growing penetration of smartphones aided by introduction of 5G enabled devices

- Rapid adoption of smart devices with integrated AI for different application usage

- Increase in demand for higher resolution video streaming and immersive gaming experience on portable devices

- Increasing development of in car infotainment systems, advanced driver assist systems (ADAS) and satellite navigation for future vehicles

- Advancement of Fog and edge computing platforms, development of Internet of Things (IoT) ecosystem

- Continuous progress in manufacturing technique for micro-processors to reduce the die size.

Apart from the short-term supply chain disruptions in the market, the long term outlook for the Application Processor market is positive and driven by sustained investment, digital transformation initiatives and rapid uptake of network-based connected devices.

Key Application Processor Market Trends

The application processor industry is experiencing tremendous shifts in technology. The changing expectations of consumers combined with advances in semiconductor design and manufacturing have made the proliferation of smart connected devices have been catalysts of key emerging directions impacting investment strategies by semiconductor companies, OEMs and technology vendors across multiple hardware categories.

One of the significant new drivers is the inclination of vendors to combine application processors and AI accelerators within the same chip. As more AI/ML neural engines and acceleration hardware are installed atop system-on-chips developers plan on using application processors to handle AI workloads. These AI-enabled processors offer an array of extra improvements from gridless image optimization and facial recognition, augmented speech/natural language assistants, intelligent power optimization to predictive words to next-generationtext generation. As the use of low latency on-device AI operations increases, privacy and data protection are reaching new heights.

Another defining effect is 5G implementation which is creating demand for blazing rapid data rates, connectivity and cloud integration. Multiple smartphone and computing device vendors have adopted cutting-edge 5G application processors enabling quality boost, cloud gaming, AR builds and streaming game experiences, high-end conferencing. With the ongoing development of worldwide 5G technology, an upgrade in processor demand across all product lines is severely anticipated.

The continued transition to smaller semiconductor process nodes and shortened gate lengths also continues to be a defining movement in the industry. The shift to demanding new generation fabrication processes such as 5, 4, 3 nm, enables reduced power, increased transistor density, optimized heat outputs and sustainable economics. This movement is particularly relevant in telecom and portable applications, where maximizing the usable operating time for mobile phones means smaller power envelopes are quite in demand.

The emergence of needs for mobile gaming development and consuming more immersive multimedia for increased demand for enhanced device specs. To capture high quality graphics, high refresh-rates and high end real-time visuals, providers are already downsizing high-wattage PC components onto their communications devices with enhanced built-on hardware, ray tracing and gaming engines.

The ongoing emergence of foldable, transforming, dual-screen smartphones and similarly flexible-laptop devices lead to new dimensions of cellular hardware development. The chipsets necessary to drive the software and user experiences embrace multithreaded jobs, adjustable displays and adaptive UI’s.

Automotive, navigation and fully-autonomous platforms is receiving a lot of applications with the latest implementation of AI platforms associated with digital cockpit, entertainment infrastructure, safety systems. This diversity of application creates additional avenues for innovation within the application processor space.

The increasing utilization of edge and cloud processing by end companies and individual users has demonstrated a greater demand for local gate data management. For many industrial, electromechanical, medicine and infrastructure apps, edge AI dedicated processing platforms are required for decreased bandwidth utilization and more timely decisions.

Based on their energy efficiency and environmentally friendly production, technology firms promote a sustainable source and a new generation of application processors. The reduction in resource exhausts addresses global regulatory demands for reducing carbon legacy impact, dovetailing with advantageous support for mobile IoT and electronics.

Several key trending behaviors are setting the precedent for the industry such as:

- Expanded use of AI/ML acceleration in app-centric processors

- Interconnection of 5G enabled applications systems and Infrastructure

- Migration to 3x, 4x, 5x nanometers architecture utilized in high-performance, low-power chips

- Promotion of gaming focused mobile processors

- Integration of holistic automotive/ADAS hybrid processing systems

- Push for edge confined AI tasks and acceleration

- Endorsement for eco-friendly application processing architectures

As a fiercely competitive, high priority on structure and extended supply chains continue to be paramount, the industry’ pushing, partnering and diversification of application processor budget has led to a natural emphasis on innovation-based excellence. Preparation to deliver design leadership with optimized smart web-enabled solutions is the upcoming challenge.

Key Application Processor Market Restraints

While the world market of application processor markets present significant growth potential, a range of restraints and operational issues currently serve to constrain market development and introduce uncertainty around the outlook for industry manufacturers, suppliers and technology adopters. These operational issues impact manufacturing capacity constraints, pricing strategies, innovation cycles and long term profitability within the worldwide semiconductor industry.

One of the most pressing operational restraints impacting the global market is the significant costs around semiconductor R&D, design and manufacturing. High quality application processor designs require large up front investments into the multiple chip and system level architecture experiments, fabrication plant investments, test equipment, software integrations, design tools and staff training. The move to smaller, more expensive logic design node process technologies such as 5nm and 3nm has escalated capital investments, putting additional strain on the global foundry manufacturing sector to meet customer volumes.

Supply chain constraints continue to present operational challenges to the computer hardware sector of the global chip industry. The interconnected world application processor value chain relies on supply chain inputs from raw material suppliers, wafer fabricators, foundry packagers, logistics management and sales to consumer OEM equipment providers. Disruptions to any segment such as those created by natural disasters, geopolitics or global health pandemics can bring the entire supply chain to a halt, with inventory shortfalls, delay to product announcements and increased manufacturing costs.

Pricing pressures continue to mount around the application processor due to competitive pressures. The major players within the market are continually battling to develop leading edge performance products at a lower cost to win against competitors. Smartphone OEMs and other consumer device tier one manufacturers execute frequent negotiating strategies for double digit reductions in component purchase prices creating operating performance margin compression across the semiconductor ecosystem. The pressure around technology obsolescence for consumer-oriented processors continues unabated.

Consumer electronics are evolving at an extraordinary pace leading to an extremely short product lifecycle and fierce innovation racing. Failing to keep pace can lead to loss of market share and shrinking product profitability. Additionally the short product development cycles of cell phones and consumer devices increase the operational complexity and risk around inventory management.

Thermal logics, power draw and power management operational issues are impacting the performance and acceptance of application processor products. As these processors become increasingly capable, especially if capable of supporting GPU, AIl and VR workloads, gaming applications, high quality multimedia and data management require their capability to increase, increasing heat generation, management and battery drain. Use of these high power processors must be balanced against heat dissipation issues in design and device performance to ensure long term reliability.

Intellectual property lawsuits and patent conflicts continue to create obstacles within the application processor value chain. Hardward related legal scuffles occur over the design of processors, communication architectures, graphics steps, general purpose processor arrays and manufacturing methods, often delaying product availability, creating additional legal expenses and increasing market discontinuities.

A key area of restraint impacting the industry is the lack of available skilled semiconductor engineers and chip designers in the overall engineering sectors. Advances in processing technology and performance enhancements demand mastery of hardware, embedded system design, usability requirements and AI architecture optimization not always obtainable from mainstream engineering talent pools.

Security issues regarding application processor Hardware architectures are rising as a potential market challenge. The individuals devices these chips go into often contain sensitive personal, financial and corporate information. Responses to hardware execution, malware defenses and cyber security can help maintain market trust.

Governments of the world are implementing increasingly strict environmental standards for the fabrication plants, water intake and waste handling and purity and chemical disposal standards in place at manufacturing facilities present future operational hurdles for the world’s global semiconductor vendors.

Key restraints impacting the global market include:

- Severe semiconductor fabrication and R&D costs

- Pressure from global supply chain related issues and component shortages

- The accelerated pace of technology obsolescence and shorter production innovation cycles

- Power management and electronic thermal management creating barriers to processor adoption

- Intentional hardware property disputes

- Global shortage of high quality, skilled semiconductor design and manufacturing personnel

- Security vulnerabilities within application processor hardware

Environmental regulatory pressures impacting the global semiconductor manufacturing sector.

The global market for application processors continues to see active investment in sales, automation, supply chain diversification and partnerships to build over the current constraints, but the long term outlook remains positive.

Application Processor Market Key Opportunities

The application processor industry is undergoing massive growth opportunities, driven by an increasing number of connected devices, artificial intelligence trends, and demand for high-performance computing applications in various industries. Application processors act as key computing platforms for smartphones, tablets, automotive infotainment systems, smart wearables, gaming platforms, and industrial automation applications. With the increasing digital transformation across the globe, manufacturers and semiconductor vendors are exploring numerous strategic opportunities to bolster their application processor industry share and technological strength.

The rise in 5G-enabled device adoption among consumers has created a promising growth opportunity for the application processors industry. As the smart device industry transitions from 4G to 5G connectivity modules, it generates a high demand for advanced application processors that offer ultra-fast data connectivity, low-latency communication and high power efficiency. Smartphone vendors are further investing in premium and mid-range 5G terminal devices, providing a favorable demand environment for advanced multicore application processors with embedded AI acceleration ability.

Artificial intelligence/ machine learning trends further boost lucrative industry opportunities for application processor market participants. Modern application processors have high-end dedicated neural processors and AI engines embedded within them for performing real-time data analysis, image detection, voice operation and progress forecasting. Such AI-embedded module performance processors are becoming standard for smartphones, smart home appliances, industrial robotics and edge computing applications.

A further opportunity is stemming from the connected vehicle industry. Autonomous car systems, driver-assist features and connected car solutions all require high-performance and computing-intensive application processors for enabling the system functionality. The automotive industry is embedding sophisticated infotainment cabins, electrical dashboards and AI-enabled safety components that heavily depend on advanced application processors. With the electric vehicle industry emerging, the demand for application processors is magnified in the presence of software-define vehicles.

The fast increase in the Internet of Things economy enables new application processor growth opportunities. Smart-living ingesting sensors, healthcare monitoring devices, industrial process automation tools and smart city utilities all rely on a minimum processing framework combined with lightweight power utilization. With the rising number of interconnected IoT units all across the globe, semiconductor firms will focus on developing compact and power-optimized application processors suited for edge computing applications.

Cloud gaming and the virtual / augmented reality industry would further create promising opportunities for application processors. The consumers demand for high-definition gaming graphics, enhanced augmented reality (AR) and virtual reality (VR) experiences is expanding the adoption of advanced processors with graphics intensive demand and low latency specifications in gaming smartphones, portable computers, auxiliary helms and so on.

The wearable devices industry has a promising growth potential for application processor vendors. Fitness tracking devices, multisensory glasses, smartwatches, and health monitoring tools look for high performance and ultra-low power consumption profile for the embedded application process threads. Consumer needs for smarter, fully functional and long-lasting powered wearables is generating further innovation in compact application processor architectures.

Emerging economies are also contributing to industry growth opportunities. The growing disposable income, expanding internet connectivity network and surging smartphone penetration levels in several areas across Asia Pacific, Latin America and Africa are providing an increased demand for consumer electronic devices. Application processor players are making strategic advances into such geographies by launching cost-effective entry level and mid-range module processors.

The transition in advanced semiconductor manufacturing technicalities is also presenting new opportunities for innovation. The evolution to smaller process nodes such as 5 nm and 3 nm enables greater transistor density, higher processing intensity and high energy efficiency. Semiconductor players that invest in next-generation manufacturing technologies can avail a competitive advantage with better performance applications.

The increased focus on strategic alliances and system collaborations can further benefit the industry players. Semiconductor firms are collaborating with smart device manufacturers, automobile companies, consumer electronics suppliers, network service providers and software developers to hasten new product development and optimize overall application processor performance across integrated platforms. This enables the industry players to broaden their technological product portfolio and increase customer outreach.

Furthermore, the surging crowd for edge AI processing applications is transforming industry rivalry. More enterprises prefer to perform data processing locally to minimize latency and maximize security and safety. This trend is boosting the development of edge-optimized application processors that can undertake artificial intelligence workloads on their respective electronics without relying too much on cloud infrastructure.

The application processor industry offers great growth potential driven by rising consumer preferences, technological advances, expanding digital data ecosystems and greater proliferation of intelligent connected tools and devices.

Application Processor Market Key Drivers

The application processor market is mainly influenced by the increasing consumption of sophisticated consumer electronics and smart connected devices across the globe. Application processors are an integral part of semiconductor devices and are responsible for the management of an operating system and multimedia, graphics, connections, and other related devices. As consumers demand faster, feature-rich and more power-efficient applications, the market for top-end processors is also witnessing strong growth.

One of the prominent application processor market trends is the escalating smartphone industry. Smartphones have become a ubiquitous part of every individual’s life. Users increasingly rely on these devices while communicating with other people, playing games, enhancing productivity, trading, and making quick payments online.

Optimized high-speed multiplayer games, high definition photography, fast internet access, and AI enabled applications demand multicore application processors that possess high-performance levels. Smartphone manufacturing firms are allocating significant resources toward Processor upgrades in a bid to stay ahead of their competitors. The booming deployment of 5G network infrastructure is another vital component of application processor market growth. 5G connectivity enables immense data transfer speed, low latency communication, and clear network reachability.

These features demand device applications to incorporate high-performing processors with integrated 5G modems and increased computational efficiency. Continued global rollout of 5G networks and accelerated manufacturer replacement cycle are thus major contributors to the growth of application processors. Demand for innovative application processors is also on the rise, fueled by the incorporation of artificial intelligence functionalities in devices.

AI-enabled applications such as voice recognition, facial recognition, translation services, and cognitively photographic applications require high processing abilities that can conduct a multitude of neural net calculations dynamically at all times. Innovative semiconductor firms are thus including AI accelerators with a specific structure dedicated to performing AI applications within processors. The upsurge in popularity for entertainment and gaming applications is another factor contributing to the proliferation of application processor demand.

Advanced thermal handling and graphics-generating capabilities are a must for video streaming or online gaming and augmented reality applications. Growing adoption of powerful application processors by the gaming community that seeks immersive and highly nuanced user experience also fuels the demand in this segment. The proliferation of the Internet of Things is yet another factor stimulating this market’s growth.

IoT applications such as smart homes, wearable gadgets, industrial automation systems, connected healthcare equipment, etc., require powerful application processors for efficient data processing management. The growing trend of IoT globally therefore results in a rise in application processor demand. Automotive digitization, which involves the modernization of vehicles with extensive infotainment content, digital cockpit, advanced navigation system, driver assisting technology, and the use of connected digital vehicles will also drive the application processor market forward.

The momentum in adoption of edge computing technologies is also a significant market influence with growing predilection for on-site storage and analysis for superior response results, lower bandwidth consumption, and deterring AI/analytics load on the central cloud structure. The technological breakthroughs in semiconductor manufacturing processes such as the progression to 7-5 nm and 3-1 nm fabrication processes, are also enhancing market growth. Thinner, better and faster devices are readily developed using these new generation processors.

Rising consumer obsession with wearable electronic devices such as watches, fitness and health trackers also stimulate market growth. The dynamic marketplaces in the application processor market is also driven by surging investments for research, development, and improving performance and architecture. Top-shelf technology firms are betting on security, graphical processing, and AI functionality within subsequent application processors. The culminating rise of the digitalization wave across global industries has a consequential impact on the growth of the application processor industry.

Application Processor Market Segment Insights

The application processor market is classified into device type, core type, application and region. Such segment wise insights and analysis provide a detailed understanding of changing consumer preferences, technological developments and industry specific demand trends, which together influence the application processor market globally.

Device-wise analysis, the smartphone segment dominated the application processor market with a significant share in recent times owing to the gigantic adoption of smart handheld devices around the world. Android smartphones require highly efficient and high speed processing units which can support multitasking operations, multimedia, gaming, applications, artificial Intelligence enabled systems, high speed internet etc. High end premium smartphones increasingly incorporate high end octa-core and application processors integrated with AI capabilities for better efficiency and performance levels.

Tablets segments are also contributing to high growth in the application processor market. The tablet terminals are mainly used for educational, entertainment, corporate work applications and remote work terminals. The increasing demand for hybridization of work from home and online learning applications has propelled the use of tablet terminals and in turn high demand for application processors which have the capacity to handle graphics and multitasking applications efficiently.

Wearable devices are also providing emerging growth opportunities for application processor manufacturers. The global consumers are witnessing increasing use of fitness and health monitoring applications, smart watches, fitness bands, augmented reality devices etc. The wearable operated devices demand application processors that provide compact design, low power consumption, integrated connectivity, embedded processing of sensors etc. High focus on improving battery efficiency and real time processing data within wearable application processors is paramount to meet consumer expectations.

Processor wise analysis. Owing to their high efficiency, the octa-core processor segment is holding the market share in application processor market. The octa-core processors support acceleration in multitasking operations, efficient gaming, faster load on applications, thermal management resulting in higher efficiency of the high end gaming and smartphones. The high end or high price premium smartphones equipped with octa-core application processors are gaining popularity in recent times.

While the quad-core processor market segment continues to enjoy increased demand owing to increasing middle-end customer demand for performance with low cost in contrast to high end devices. The quad-core processors are ideal for standard smartphone applications, streaming, browsing, normal entertainment applications, moderate gaming etc. The entry level gadgets and low cost consumer electronics use mid or entry level quad-core processors in the design.

The demand from dual-core processors is reducing gradually as the computing needs are increasing along with various consumer applications. Though dual-core processors are used in basic gadgets and low cost/entry level consumer products. They are also used in low powering wearable IoT applications and low power embedded devices.

Application wise analysis, Consumption of application processors for consumer electronics Equipment dominated the application processor market for its utilization in various consumer personal, entertainment, computing devices. The consumer electronic products have witnessed continuity of adoption even through the transition from analog to digital equipments, multimedia content revolution, large screen high definition displays, AI plug-in units, multi-featured camera phones and still remain the foremost purchaser of high performing high capacity application processors.

Automobiles are witnessing revolutions in digital content and automation concepts. The digital content provision and demand from different car systems like the Navigation devices, infotainment systems, autonomous drivers, and digital instrument clusters are the main contributors of building demand for application processors. The huge adoption of electric vehicles and software defined vehicles will further boost up the processor demand.

The industrial automation sector consumes high number of application processors by way of deploying smart systems of automation, robotics, industrial IOT, predictive maintenance and machine learning etc. Increasing demand for these high accuracy systems will provide further expansion potential for application processor market.

Region wise analysis, The largest share of application processor market is in Asia-Pacific region owing to the presence of huge number of smartphone makers, semiconductor manufacturing units, personal electronics industry etc. The booming disposable income levels, digital penetration, changing lifestyle of the consumer base provides highest demand for consumer electronics processors of various kinds like personal entertainment devices, mobile and digital content provision gadgets etc.

North America, having good technological infrastructure and having highest demand for premium gadgets and digital systems, is providing huge market share for application processors. Europe too accounts to a significant share of application processor market supported by activities related to automotive digitalization and industrial automation. Thus, the market for application processor is mushrooming owing to technological advancement, increasing usage of connected devices, and rising consumer preference for digital ecosystems across industries.

Application Processor Market Regional Analysis

The global application processor market has observed a robust growth and is expected to grow steadily in the coming years with a rise in number of smart consumer electronics, autonomous vehicles, digital transformation within the automotive industry and the advancement in artificial intelligence.

Application processors are an advanced semiconductor chip used in controlling computing functions of mobile devices such as smartphones, tablets, wearables, in-car entertainment devices and game consoles and IoT devices. With the increasing demand for energy efficient, graphics intensive, high performance processing power across varied consumer electronics and automotive applications, the market is experiencing an acceleration across the global regions.

The market in North America is one of the most sophisticated ones and the focus of semiconductor makers in designing and developing innovative semiconductor architecture. Being the hub of various major semiconductor manufactures the market in the North American region leverages its cutting-edge research and development infrastructure and an increasing influx of capital investments in building up the artificial intelligence-enabled computational power across devices.

The United States led the growth in the region owing to the surging demand for premium smartphones, hybrid as well as autonomous vehicles, edge computation platforms, and cloud-connected home appliances. The rapid widespread proliferation of the 5G network and connected devices at the consumer level, adoption of smart homes and the surge in data-assembly intensive applications, virtual gaming as well as AR capabilities are driving the demand across.

Europe’s market witnesses a steady rise primarily due to increasing innovation within the automotive sector and industrial digital transformation push. Automotive OEMs and electronics manufacturing players are implementing smarter processors in their infotainment consoles and integrating it with hybrid as well as electric vehicles and IoT enabled industrial applications.

Decreased power consumption levels of electronic devices and adoption of smart manufacturing processes enhance the market growth for application processors. The increasing number of smart manufacturing initiatives and burgeoning consumer electronics market further propel the semiconductor manufacturers across the region.

The Asia-Pacific region holds a pole position across all the regions and is expected to achieve the fastest growth over the forecast years. The region has one of the most prolific electronics manufacturing hubs spread across China, South Korea, Taiwan, and Japan and thus contributes heavily to the rising adoption of high-performance application processors across emerging economies coupled with increasing urbanization and purchasing power of the middle-class population. China is one of the prominent countries with massive investments from top tier players in the burgeoning semiconductor industry coupled with its locally available semiconductor manufacturing capacity.

South Korea and Taiwan, with their robust semiconductor manufacturing base contribute significantly to the growth across the region while the Indian market is expected to be a promising one, propelled by massive usage of smartphones, expanding internet penetration and policy push for domestic electronics manufacturing.

Moderate growth is estimated over the forecast years across the Latin America region with increase in the usage of connected electronics at a broader level and widespread adoption of smart and digital solutions and devices in the region. The region’s potential is amplified with an increasing trend of digital technology adoption despite some constraints in the supply chain within the semiconductor industry.

Middle East & Africa region, over the forecast years are predicted to gain moderate growth owing to increasing smartphone penetration, growing telecom infrastructure, and the smart cities initiative. The G.C.C. States within Middle East & Africa are expected to invest significantly in digitizing and futuristic network connectivity infrastructure. Increasing awareness of connected healthcare, smart home appliances, AI enabled consumer electronics and gadgets, which will directly boost up demand for application processors across the regions.

Overall, all the above-mentioned segments across different regions witness significant rise due to various technological innovations incorporating the advanced electronic solutions powered by AI, machine learning, deep graphics logic, and low power consumption to meet the rapidly growing high-speed mobile computing, automation, and smart connected devices need.

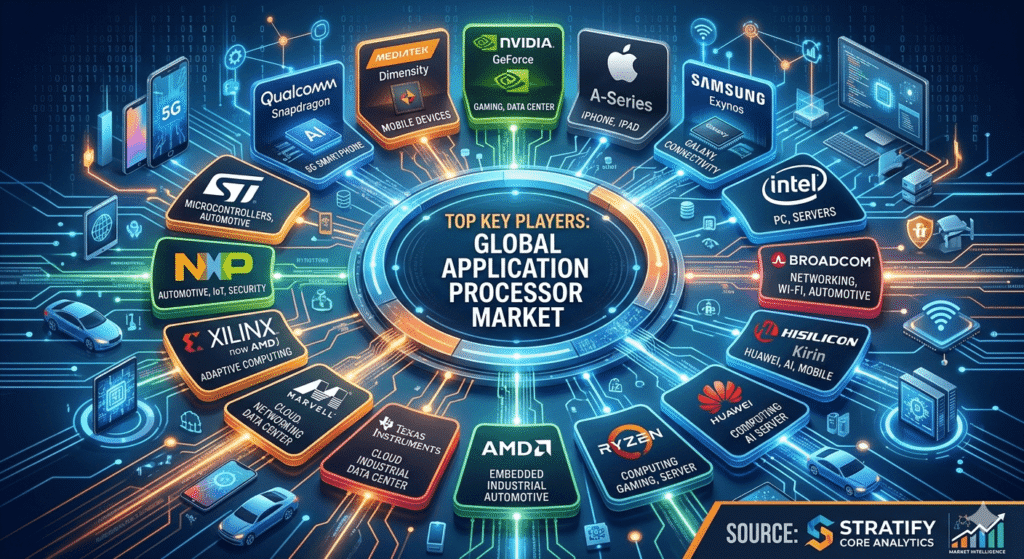

Top Key Players operating in the Application Processor Market

- Qualcomm Incorporated

- MediaTek Inc.

- NVIDIA Corporation

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Broadcom Inc.

- HiSilicon Technologies Co., Ltd.

- Advanced Micro Devices, Inc. (AMD)

- Texas Instruments Inc.

- Marvell Technology Group Ltd.

- Lattice Semiconductor Corporation

- Xilinx, Inc. (now part of AMD)

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

The application processor competition is so fierce that advances in product design, AI acceleration, next-generation chip architecture and low-power computing have become the focus of the industry. Most of the key players in the market would be able to fund R&D activities to unveil application processors that support machine learning, AR/VR, high-end gaming, autonomous drive systems and real-time data analytics.

The adoption of strategic alliances, acquisitions and mergers among the industry players would continue to take place as they strive to ramp up chip manufacturing capacity and expand their global market presence. The competition among chipset manufacturers would further fuel the development of 5G enabled processors, edge AI computing and multi-core processor technology. Meanwhile, rising investments in semiconductor manufacturing plants and advanced packaging will likely change the industry competition scenario in the coming years.

Additionally, intensifying geopolitics, breaks in the semiconductor supply chain and surging government investment in the domestic chip manufacturing capacity could enhance the focus on semiconductor self-sufficiency, thereby escalating the competition among the worldwide application processor vendors.

FAQ

1. What is an application processor?

An application processor is a semiconductor chip designed to manage computing operations in electronic devices such as smartphones, tablets, wearable devices, automotive infotainment systems, and IoT products.

2. What factors are driving the growth of the application processor market?

The market is primarily driven by increasing smartphone adoption, rising demand for AI-enabled devices, expansion of 5G technology, growth in connected IoT ecosystems, and advancements in mobile gaming and multimedia applications.

3. Which region dominates the application processor market?

Asia-Pacific currently dominates the application processor market due to strong electronics manufacturing capabilities, high smartphone penetration, and significant semiconductor investments in countries such as China, Taiwan, South Korea, and Japan.

4. What are the major challenges in the application processor market?

Key challenges include semiconductor supply chain disruptions, high manufacturing costs, rapid technological changes, geopolitical trade restrictions, and increasing competition among global chipset manufacturers.