Global Trade Credit Insurance Market Overview

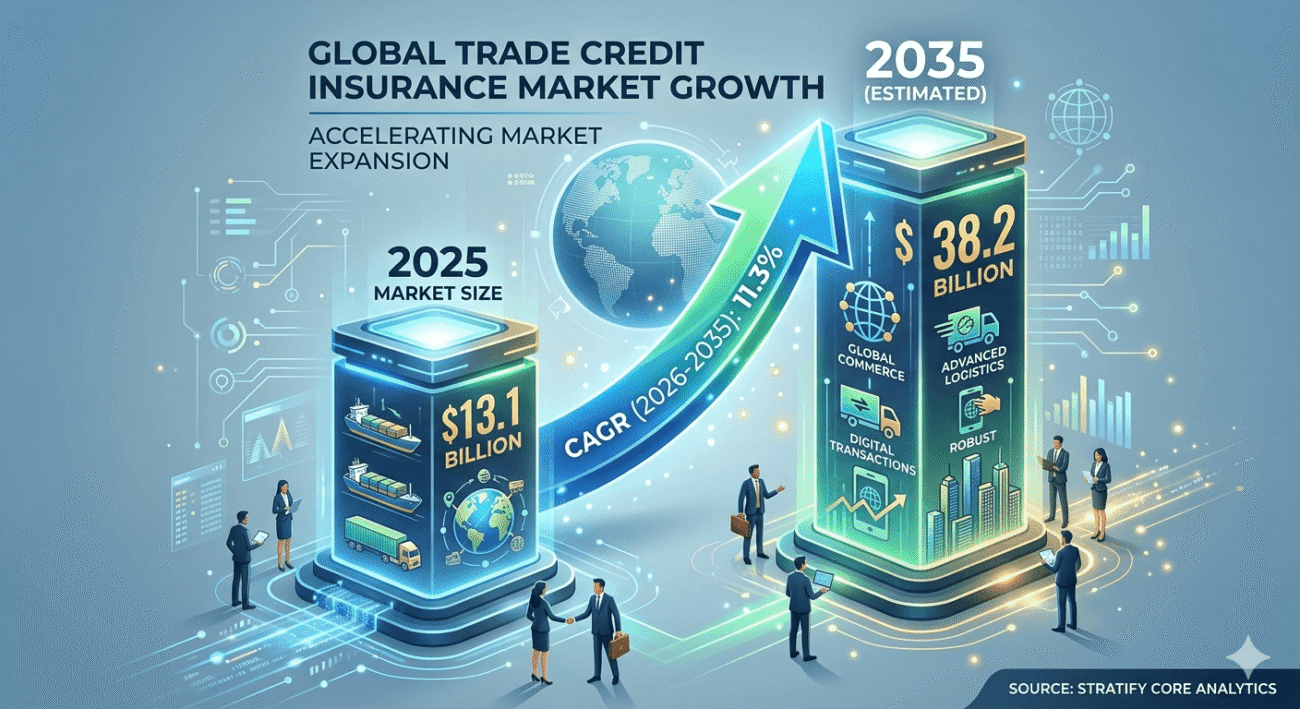

The trade credit insurance market size was $13.1 billion in 2025 & is expected to reach $38.2 billion by 2035 at a CAGR of 11.3% from 2026 to 2035. The global trade credit insurance market is a segment of international trade and a tool for financial risk management. Trade credit insurance is a risk management tool that assists enterprises by protecting against trade losses resulting from nonpayment of trade debts by them, be it due to numerous reasons, including insolvency, bankruptcy or financial crisis, or because the trading partner is facing problems.

As the trade networks become intertwined and deeply integrated, the businesses, especially those operating in industries like manufacturing, retail, construction, and automotive, are demanding trade credit insurance to safeguard their cash flows so that their business operations are not hampered. The parameters of the market keep switching and evolving but trade credit insurance will stay one of the most important facets of international trade for the risk cover it provides to the trades. In a broader sense, the trade credit insurance market globally is a part and one of the critical components of the international trade and financial risk management system.

Trade credit insurance has always played an extremely significant role in reducing the nonpayment risk of cross border trade transactions. The companies have always extended the period to their respective customers to pay their outstanding bills because it maximizes their sales in the event of keeping their customer base satisfied. But the fact remains that if some of the customers fail to make payments, the cash flows and profitability of the companies will be impaired.

This is where a trade credit insurance channel steps in. The risk is being mitigated and so the companies can invest wholeheartedly with confidence in each other. The growth of the market today worldwide itself is driven by factors like acceleration of globalization, increase in the number of exports and the realization of firms of nonpayment risks and consequently a realization of the need of trade credit insurance as part of their risk mitigation strategy for international trade.

In other words, the trade credit insurance is nearing a field of universal acceptance among companies, from gigantic multinationals to small and medium enterprises. The factors responsible for the growth of the market worldwide include global mega trends of technological upheaval, macro-economic risks being frozen in the low, low inflation environment, and zero interest rate environment, the cyclical upswing and the supply chain bottlenecks amongst others. As the exportoriented companies keep expanding their companies levels of exports, the macroeconomic risks are on the rise with them into the markets which further has accentuated the need for trade credit insurance services.

This trend is expected to continue forever and the trade credit insurance is here to stay. The technological developments like use of advanced analytics, artificial intelligence and machine learning are directing the insurance market to its new destination. The new technologies may be revolutionizing credit risk assessment and the monitoring of risks in real time.

Insurance carriers with an edge will be able to pinpoint the credit risk more efficiently and respond faster to developing situations that affect the risk rating of the insured business; this can result in more accurate pricing of policies and fewer requirements in processing payments. The new platforms created by insurance companies are expected to wield new supports for small and medium enterprises in most buoyant trade credit insurance market. The economic troubles like global economic slowdown, rising geopolitical tensions & risks, inflation, supply chain disruptions, emerging market slowdown are also indicative of a positive business sentiment, which led to demand for trade credit insurance services. Macroeconomic and geo-politic developments, like trade conflict, rising sanctions, currency fluctuation gradually erode the ability of the buyers to meet their payment obligations which is viewed as a business development coupled with a rise in the demand for trade credit insurance services.

The banks and financial institutions also welcome trade credit insurance because of a reduction in the risk of making or providing funds and loans to the protected enterprises. Also, many governments strongly support this market as part of their assured support to their respective exporting companies. The supported, government-backed, trade credit insurance agencies promote the confidence of the exporters to dare and participate in aggressive exporting to various foreign countries and provide backstop to the base trade credit providers like banks and specialized financial institutions.

Countries coming under the precinct of fast developing APAC region, including China, India, Japan, and South Korea etc. are getting rapidly involved into international trade and investments fetching the region a favorable trait for its uniform development. The GE market is segmented into, by basis for segmentation into, by type of policy, application and geography analysis. In terms of share of big firms, they prefer to acquire turnover policies to take care of their entire portfolio of customers, while the small and medium enterprises constitute a predominant growing segment of the trade credit insurance market as more agencies are offering more flexible and affordable policies to cater to their requirements.

With respect to geography, Europe has an established trade credit insurance market built into it and a large number of its companies are already trading on trade credit insurance basis. North America region is also on the faster rise of the trade credit insurance demand and adoption by more companies is about to happen de facto. But the apex opportunity for the market is with the APAC region which promises a robust growth at a faster pace due to heightened requirements of industrialization, global exports and a greater number of businesses raising towards the higher entity trading in the entire world.

Countries like China, India, Japan, and South Korea etc. are coming to the forefront quickly in the trade credit insurance domain. The global trade credit insurance market however is faced with intense competition between many insurance providers. This competition is focused on an outward expansion by client acquisitions, keeping in under existing client portfolio, by partnering with other firms so as to explore newer underpenetrated markets, by mergers and acquisitions and by expanding scope with the technological advancements.

The current forward thrust of the competition in the trade credit insurance market is taking a direction towards investments in technology and digital portals so that the trade credit insurance services are aesthetically received by other companies. There is also an initiative by the market players to bring specialized industry-specific policies in trade credit insurance market. Globalization and the associated expansion of international trade are expected to be evident in the number of businesses worldwide.

The market for trade credit insurance has a promising future establishment as it has a sustained, longterm root in the global trade networks and companies will need to protect themselves against the mounting risks only to continue to do business on a go ahead basis.

Key Trade Credit Insurance Market Trends

The global trade credit insurance industry is experiencing several emerging market trends driven by changes in international trade, advances in technology, and the increasing desire of businesses to efficiently and effectively manage their risk. Among these trends, the most overt is the rising level of digitalization within underwriting, claims processing, and customer service functions. Many insurance companies are adopting artificial intelligence, predictive analytics, and big data mining methodologies to determine the credit ability of buyers as well as the propensity of specific customers to default on payments. These innovations enable insurers to analyze large quantities of transactional and financial data quickly and process this information and come to decisions in real-time, allowing for more nimble and accurate risk analysis.

Also notable is the increasing utilization of trade credit insurance by smaller firms and medium-sized enterprises compared to the past. Traditionally, trade credit insurance was deployed by large multi-national companies given the policy complications and prohibitive premiums. However, the industry is now developing more streamlined coverage as well as flexible, lower premium policy options targeted at now-underserved SME customers. Digital onboarding and simplified policy management solutions are breaking down the barriers to entry faced by much of the SMB sector, emphasizing the vital role of trade credit cover in protecting companies’ cash flows and minimizing exposure to bad debt, particularly in an uncertain economy.

An associated issue impacting the past and present activities of the trade credit industry is the proliferation of global supply chains. From accelerated adoption of cross-border trade to the rise of multi-national companies processing a diverse set of customers in multiple markets, exposure to new and complex political and commercial risks has increased. Trade credit insurance policies have expanded their coverage parameters accordingly, offering protection against political risk, market collapse, and the impact of currency rises and falls. Especially in relation to exports into emerging markets, cross-border coverage is in higher demand.

Related to this trend is the increased influence of environmental, social, and governance considerations upon underwriting decisions across the industry. Many insurers now factor in the sustainability of their insured’s business model and operational practices during the underwriting process. As such, ESG performs an increasing role in the selection or rejection of insured customers based on their perceived strength and resilience over a long-term horizon. At the same time, the industry is raising its own stakes in terms of its sustainable practices and reducing the scope of its exposure to high statutory or external risk industries in the present day.

Another expansion occurring within the trade credit insurance industry involves the increased synergy with the banking and broader financial services industries. Insured receivables are becoming an ingredient in risk mitigation strategies undertaken by financial institutions in regard to implementing working capital finance solutions. Commercial lending or export financing can be secured more effectively, while the market is more willing to embrace integrated financing/insurance solutions such as factoring, supply chain finance, and loan off-take options that protect both the trade insured and the commercial lender or funder.

One further trend impacting the market today and definitely expected to influence the industry going forward is demand for sectorally-specific, customized solutions. Certain industries, for instance, automobiles, chemicals, pharmaceuticals, and electronics, operate according to long lead times and/or unpredictable developmental and regulatory calendars. As a result, they tend to experience relatively unpredictable payment patterns and a greater degree of market volatility. Trade credit policies that are customized toward these specific fields can allow businesses within these sectors to reduce their individual credit risk and better meet customer demand.

Lastly, a key feature of the current market environment is the rising amount of geopolitical instability in the world today. With increased predilection for trade sanctions as well as disruptions to supply at the hands of political instability, global conflicts, natural disasters, and supply side shocks have driven many businesses to adopt a more conservative appetite for international growth. Furthermore, trade credit insurance coverage is more frequently purchased in conjunction with political risk policies that protect against the political and legal risks impacting exporting organizations into various markets, especially volatile or emerging regions.

Finally, a non-traditional phenomenon influencing the present face of the trade credit insurance industry is a growing demand for real-time, integrated, monitoring tools from customers. Companies have developed a greater appetite for constantly tracking the health of their current buyer base using sophisticated digital solutions. Insurers offer a series of tailored dashboards, reporting engines, and alerts that inform companies when buyer financial condition has deteriorated and provides alerted events, thereby enhancing every company’s ability to proactively manage credit exposure and make more informed trade decision in today’s interconnected world.

Overall, the global trade credit industry is evolving toward a more technology-enabled, customer-centric, and globally complex paradigm. The rising integration of digital tools, the emergence of more SME-friendly products, expanding cross border trade coverage, and consideration of more factors (be it ESG or geopolitical risk) offer opportunities for insurers to stay ahead of this rapidly-changing landscape.

Key Trade Credit Insurance Market Key Restraints

While the global trade credit insurance industry is poised for promising future development, several restraints exist to hinder the expansion of trade credit insurance policy adoption both on a broad industry level and at regional levels. One of the biggest restraints preventing the development of the trade credit insurance industry is the high retail price of premiums charged, which makes the policy unviable for both businesses and underwriters. Premiums are generally charged at levels determined by the underlying risk profile and factors such as buyer risk, industry volatility, geographic concentration and macroeconomic health are taken into account. For this reason, smaller companies utilizing potentially inadequate trade lines believe the costs are not justified given their modest margins and working capital base, and many of these firms choose to remain uninsured despite high receivable risks.

Another factor restricting the growth of the trade credit insurance industry is the complexity of policy structures and coverage defined in such policies. Many trade credit insurance purchase transactions involve detailed underwriting information requirements, various coverage exclusions/deductibles/waiting periods/claim criteria and intricate provisions that are often difficult for many organizations to understand. Particularly for small businesses without dedicated credit management teams, it can be difficult to compare and evaluate policy coverage terms, and organizations that fail to understand the policy terms may be unsatisfied with the policy coverage during the claims settlement stage.

The current macroeconomic market situation and economic uncertainty can also add to the operational liabilities faced by underwriters. During recessionary, inflationary or high company failure market periods, there is a surging flow of claims and underwriters face an uncertain risk posed by high claim levels and rising financial liabilities. In response, underwriters tend to tighten underwriting standards, cut back coverage and increase premiums which affects future accessibility of the product when businesses face the highest demand. The cyclical nature of insurance underwriting can in turn make product adoption unfeasible for certain customer segments.

Availability of accurate credit data is an issue in many developing and emerging economies, resulting in the confirmation of large provisions of trading data by a lack of formal accounting statements, weak government oversight of financial disclosure, inconsistencies in available documents and a general lack of macro-economic transparency. Such deficiencies in available trader information heighten the information asymmetry and insurance exposure and the mismatched elements can limit insurers’ appetite to provide coverage in these regions.

Trade credit insurance can also be hindered by an uncertain political environment and fluctuating regulations. Trade protection measures, trade agreements, sanctions, cross-border taxation and compliance rules are regularly adjusting to new trade standards, and this shift in operating rules limits available lines of credit, increases operating costs and increases the chance of account failures. An unstable political climate within certain regional block also raises claim risk in such areas and make insurers reluctant to operate in such markets.

Another restraint faced by the industry is the process and time required in claims settlement. The payments received by organizations that have suffered trade default are often required to be used as working capital to allow for operational continuation, but lengthy claim investigation and document review before payout can be frustrating for customer relationships. Many customers in this situation require immediate liquidity support, and an over-complicated claims process can tarnish the insurers friendly customer-facing reputation.

The presentation of other, newer means of risk mitigation has also inevitably led to major competition for the trade credit insurance industry through the growth of collateral security, internal credit controls, invoice factoring, letters of credit, diversified trading and self-insurance. Larger organizations, notably those with solid finances and minimal borrower groups, often employ self-insurance strategies rather than disbursing regular premiums to insurance providers. Moreover, these alternatives become more attractive in times of economic downturn and constraints within the economy.

A lack of awareness can hinder the future growth of the trade credit insurance market, especially for customers in developing countries outside of broad industry knowledge bases. Many businesses lack an understanding of the inherent operational and financial benefits of trade credit insurance policies, and this dearth of knowledge results in disparate uptake. Insurers continue to face the ongoing challenge to educate potential customers and foster familiarity with receivables risk management techniques.

New technological developments and the increasing prevalence of online data systems have created potential cybersecurity risks within the trade credit insurance market. Attempts at system hacking, botNET attacks and data theft can cause major reputational damage, reputational damage and regulatory issues in a market where large volumes of sensitive financial information are stored and managed. As insurers transition to more high-speed digital customer platforms, cyber threats result in a greater likelihood of system downtime and service interruption, creating operational difficulties.

Concentrating exposure to one industry sector can result in risk concentration, and underwriters who suffer large claims from a particular industry may be reluctant to operate within that region regardless of current strong risk mitigation techniques. Sectors such as retail, shipping, commodities and construction are prone to economic swings and the switching between boom and bust cycles, and the large scale bankruptcies that result may limit insurer value in the specific region or industry, requiring the providers to impose more considerable restrictions.

Although the trade credit insurance industry is forecast to grow with strong long term prospects, the industry will continue to have to contend with diverse restraints that will affect product development and customer uptake. The most prominent reactions will remain a high premium value, more complex policy design, low levels of general awareness and a highly cyclical “boom-bust” upswing/downswing cycle, which in turn, within certain client segments, inhibit the targeted long term growth opportunity.

Trade Credit Insurance Market Key Opportunities

The worldwide demand for trade credit insurance solutions represents a considerable business growth opportunity for market participants due to robust requirements of companies from every industry segment to seek more reliable ways of protection against payment defaults, insolvency risk and socio-political uncertainty. Trade credit insurance has transitioned from a specialized financial product to a strategic tool of risk management, providing for expansion of operations in a safe manner and managing a healthy cash flow. Modern globalized economy, digital trade proliferation and a volatile macroeconomic climate determine a positive environment for the creation of a broad array of innovative insurance solutions, relevant for constantly evolving business needs.

One of the main opportunities in the trade credit insurance market is the swift growth of global trade activity, as companies tend to establish new operations internationally to diversify revenues and penetrate new markets. Transition towards international trade makes businesses more exposed to the risk of late payment, non delivery, currency fluctuations and political upheaval. The insurance of accounts receivable allows exporters and suppliers to mitigate these risks. Constant increase of the global trade volume implies broad scope of commercial insurance coverage options for exporters, manufacturers, wholesalers and distributors.

Proliferation of trade credit protection among small and medium-sized business represents another relevant avenue for growth. Previously the dominant consumer of commercial credit insurance solutions were large corporations with significant international trade exposure. Currently more companies from small and medium size segments notice the advantages of insured receivables, improved credit management, and choose to build a competitive advantage by using credit insurance. Small and medium sized clients, by definition have more limited working capital and are more vulnerable to customer default. Trade credit insurance facilitates quicker access to bank financing and business continuity under conjonctural insecurities. To attract these targeted customers, insurers are designing tailored, affordable and flexible solutions for emerging markets.

Another relevant factor supporting the expansion of insurance market is the digital revolution in world financial services sector as the cutting-edge analytics provided through the application of artificial intelligence, 3D modelling, photo recognition tools, machine learning algorithms and real-time Big Data processing allow for more efficient risk assessment and underwriting. Modern trade credit insurance portfolio management becomes more streamlined as institutions are able to utilize sophisticated digital platforms to facilitate policy issuance, claim management and payment with a further increase in efficiency and better customer interaction. These factors collectively support the overall penetration of the insurance into broader business use.

The availability of credit insurance coverage helps build supply chain resilience, as enterprises tend to adapt more dynamically to disruptions induced by geopolitical conflicts, pandemic threats, inflation shocks or logistic bottlenecks. Business continuity planning and improved receivables protection imply a significant demand for advanced solutions that secure procurement, supplier engagement and logistics process efficiency.

Accelerating growth of e-business and digital B2b marketplace transactions enhances the volume of receivables generated with increasing needs for cyber security and trade protection solutions. Digital businesses of today are relatively more exposed to defaults as the transactions often take place between anonymous parties. The credit insurance allows for operating at a higher level of feedback and trade volume density with diminishing credit risks.

Emerging economies currently demonstrate considerable potential for the expansion of trade credit insurance solutions due to rapid industrialization, increased exporting activity and an evolving perception of financial risk management mechanisms. Countries of APAC, Latin America, Middle East and Africa are rapidly developing their infrastructure and increasing their trade flows. Companies operating within these emerging markets possess an improved perception of the importance of insurers‘ receivables protection and continuously demonstrate a readiness to enter innovative markets and offer new solutions.

Another area for business growth is formed by strategic partnerships of market players with external financial institutions and technology providers. Financial institutions tend to use trade credit insurance as a part of trade finance solutions to mitigate commercial lending risks and develop working capital packages. Commercial banks tend to engage in this type of cooperation since they prefer to lend against insured payables, thus increasing the overall business viability. Fintech franchisees make an important contribution with innovative automation of real-time credit monitoring processes and streamlined digital insurance policy management.

- Expansion of international trade

- Growing prospects for adoption within small and medium-sized customers

- Using digital technologies in risk assessment and payments

- Enhancing supply chain resilience

- Merits of digital trade processes

- Opportunity for expansion in emerging markets

- Opportunities for synergy with financial institutions

- Opportunities through integration with fintech sector

Trade Credit Insurance Market Key Drivers

The market is being propelled by several factors including economic uncertainties, rise in trade activities and increasing awareness about financial risk management. Companies across various industries face an increasing level of challenges related to customer insolvency, late payments and supply chain disruptions. To address these challenges, companies across the world are adopting trade credit insurance policies to secure their accounts receivable. Increasing utilization of credit insurance policies to facilitate safe domestic and international trade conduct is aiding growth in the market.

One of the key factors fueling the growth in the trade credit insurance market is the growing number of payment defaults and corporate bankruptcies. It is observed that economic uncertainties, inflation, variations in interest rates as well as geopolitical conflicts have led to increased financial pressure across industries. Companies providing trade credit to their customers face a substantial risk of significant losses resulting from non-liquidating accounts receivable. Trade credit insurance provides financial compensation in the event of default by a buyer and enables organizations to moderate cash flows and decrease receivables. The record rise in demand for financial insurance among uncertain political as well as economic conditions is one of the reasons behind growth in market share.

In addition to this, the increase in global trade and exports is also a key factor fueling expansion of this market. To cater to the ever increasing needs of new customer bases and markets, businesses are expanding their horizon to international trade. International trade projects several risks including exchange rate fluctuations, political instabilities, etc., which create uncertainty for businesses in their operations. Consequently, trade credit insurance is witnessing increased adoption in cases of export trading. In addition, a number of nations are employing export credit agencies and export credit insurance programs in support of export expansion.

Increasing focus on working capital management is further boosting the market demand. Availability of ample cash flows is necessary for supporting production activities, investments and expansion orders. A negative cash flow caused by a delay in customer payments can cause a serious impact on supply chains and overall liquidity. Trade credit insurance boosts receivable management and collateralizes receivables thus securing cash flows. Most banks and financial institutions are providing financing against insured receivables thus enabling companies to improve their borrowing capacity and better manage their cash flow.

Rapid digitization in the insurance sector is another contributing factor for growth in the trade credit insurance market. Adoption of new technologies such as cloud computing, artificial intelligence, etc. are improving underwriting and risk monitoring capabilities which help insurers in a more accurate assessment of customer creditworthiness and overcoming potential market data limitations. Digital claims management solutions and customer portals enable insurers to automate most of the operational processes thus increasing the overall efficiency of the entire process. The growth in the adoption of the latest technologies is responsible for making credit insurance easy to approach even for small and medium businesses.

Rising awareness in small to medium enterprises regarding credit risk management is a broad based factor contributing to market growth. Small and medium sized businesses are more vulnerable than their large counterparts to economic losses caused by unpaid invoices, simply due to their limited cash reserves. As awareness regarding the benefits of trade credit insurance increases, these policies are being adopted to enhance their financial stability. Many insurance providers are launching tailored products, which are customizable as per their size, and cost structure, in an effort to meet consumer needs effectively.

Supply chain issues caused by sudden supply shocks are further boosting the demand for trade credit insurance. The unintended consequences of global disruptions such as pandemics, natural calamities, geopolitical conflicts, and transportation disruptions have increased the paradigm of supply chain vulnerabilities. Therefore, even businesses these days are more focused on strengthening the supply chain management and exploring efficient supplier credits to manage their company’s supplier risks. Resultantly, trade credit insurance serves to reduce the company’s supply chain induced payment risks.

Government support and regulation related initiatives are also progressing the growth in the trade credit insurance market. Many governments are facilitating export-led growth and stability by extending support to trade finance and export credit insurance programs. Public-private partnerships and expedient regulatory environment thus, helps in providing insured trade finance more efficiently.

The factors such as increasing lack of payment security, growing global trade and export activities, increasing focus on working capital management, consistent adoption of innovative technology solutions in credit insurance operations, increasing SME awareness about credit protection solutions and supply chain disruptions along with support of government bodies are major factors aiding the growth of this market. In the duration to come, the market is expected to grow exponentially owing to the aforementioned factors.

Trade Credit Insurance Market Segment Insights

The trade credit insurance market is segmented on the basis of component, enterprise size, coverage type, application, end-user industry and regions. This segmentation analysis highlights the value of market components, consumer behavior, and growth opportunities in different business parameters. Growing trade activities, changing business practices, and technological innovations are impacting the performance of each segment.

Based on component, the market is divided into component and support services. The component segment is further sub segmented into policy purchase and policy claim management. The high adoption rate of policy purchase is attributed to the increasing use of innovative support services. Support services sub segment is further categorized into enterprise, policy and claim management applications. Policy management and claim handling (business transaction evaluation, adjusters, and others) are expected to grow at highest CAGR among all support services due to the fast adoption of digitization practices.

By enterprise size, large enterprises is expected to dominate the trade credit insurance market over the forecast period. The large companies are more significantly exposed to domestic and cross border business risks as they operate across different geographies. Large businesses significantly leverage global supply chains and demand for advanced receivable protection and risk mitigation techniques. Conversely, small and medium-sized enterprise segment is foreseen to grow very fast during the forecast period. Growing awareness of cash flow management, credit risk mitigation, and working capital support is leading to the significant adoption of trade credit insurance by small and medium-sized enterprises.

According to coverage type, whole turnover coverage, single-buyer coverage, and key account coverage are the common market segments. World turnover coverage is foreseen to held a prominent share of the trade credit insurance market during the forecast period because this type of coverage protects the organization’s entire portfolio of trade receivables. The widely adopted by big organizations with large number of clients and a multitude of transactions, whole turnover coverage is expected to grow at fastest rate. Single-buyer coverage type a gaining dominance among businesses operating in high-value and risky markets beset with concentrated buyer risk. Key account coverage type is further spilt into individual and several accounts coverage.

On the application basis, export trade and domestic trade present the dominating market segments. The export trade segment is foreseen to contribute substantially in the market share owing to the growing number of international commerce deals. Exporters and international traders face higher risks due to political instability, importer depositor insolvency and delays in payments, trade credit insurance provides confidence for enrollment into new global markets while mitigating burdensome spending liabilities. Growing domestic trade coverage in developing economies is further supportive to market expansion owing to heightened insolvency and delays in payment risk in local markets.

Based on industry, the manufacturing segment is anticipated to record the maximum contribution to the overall trade credit insurance market throughout the forecast period. Manufacturers offers short-term credit to their intermediaries, wholesalers or merchants, resulting in trade receivable risks. Trade credit insurance offers stability to their cash flows and sustains their supply chain activities. The wholesale/retail industry is also expected to demonstrate maximum contribution to the market share during the forecast period owing to massive number of transactions and high dependence on customer payments.

The agricultural pesticides industry is likely to consider the large trading volume, high reliance over receivables, risky product category and emerging auto trading industry. Other industrial sectors such as chemicals, electronic devices, pharmaceuticals and energy are also expected to contribute significantly towards total market share owing to increasing transactional complexities and demand for outputs amidst increasing credit payment uncertainties.

Regionally, Europe is anticipated to secure maximum share of the trade credit insurance market in 2014 due to sufficient operational infrastructure, high penetration in exports and smooth availability of insurance covers. Large corporate and export-oriented organizations from countries such as Germany, France and UK are also contributing to large share of the Europe regional segment. North America is also expected to grow positively, supported by increasing risk management practices coupled with the utilization of credit data sources and advanced technological platforms.

The fastest emerging trade credit insurance regional segment is likely to be Asia-Pacific owing to the rapid industrialization, rising manufacturing strength and increasing export mandates in countries like Japan, India, China and South Korea. Growing technological advancements, economic landscape, and process outsoucring for trade data management and risk assessment are also supporting regional market growth. Latin America and MEA are also foreseen to offer huge opportunity for regional growth owing to heavily growing trade activities and upgraded logistical & trade infrastructure.

- Organic growth is primarily driven by the wide adoption of whole turnover coverage because of complete receivables protection

- Technological enhancements are mainstream in policy systems and claims administration of digital platforms

- Growing incidences of commercial insolvencies and global economic uncertainties are positively

- Providing fundamental support to trade credit insurance adoption

Overall, the trade credit insurance market demonstrates extensive penetration across machine sizes and industry sub-segments. The continuous importance of receivable protection for commercial sustainability across regions is motivating the market towards robust growth over the forecast period.

Trade Credit Insurance Market Regional Analysis

The global trade credit insurance market is steadily growing, driven by increasing emphasis on protection against payment defaults, insolvencies and political uncertainties. The market facilitates suppliers and exporters from payment risks by their customers, thus helping them to maintain consistent cash flow and expand to new domestic and international markets. Increasing globalization, a volatile economy and increasing bankruptcy among companies is driving the demand for trade credit insurance.

North America is one of the leading regions in the market for trade credit insurance owing to the increased penetration and prevalence of multinational corporations. The United States is a major player in the region because most of the businesses have started adopting insurance solutions for protection of their receivables and limiting the risks of commercial transactions. The expanding trade agreements between US and Mexico are driving the demand for trade credit insurance. Due to increasing trade and increasing small and medium enterprises it would be a growing market.

Europe is one of the established markets for trade credit insurance. Major players in the market for trade credit insurance are Germany, Italy, France and United Kingdom due to increased exports and established markets for manufacturing industry, automotive industry, chemical industry and retail industry. European insurers have long presence in providing insurance solutions for different industries. Market demand is growing because of stable economic environment and stringent financial policies. It is also benefiting from growing insurance uptake for trade credit insurance owing to political tensions and rising inflation.

The Asia Pacific market for trade credit insurance is expected to experience rapid growth during the forecast period. China and India hold a major share of this market due to their growing exports. Industrial growth in countries like Japan and South Korea is contributing to market growth. Due to high cross border transactions and demand for trade credit insurance for protecting overseas payments of exporters from their customers, it has an upper hand in the global market for trade credit insurance.

China is the major market for trade credit insurance in Asia Pacific region because it is a dominant global exporter. It holds significant market share because of a huge manufacturing base. Japan and South Korea are leading markets due to a significant trade relations between the countries and well established manufacturing base. Emerging markets in Southeast Asia are performing well and would emerge as major markets owing to increasing investment from various countries. India also holds huge market potential owing to increase in MSME sector and the e-commerce and manufacturing sectors.

Latin America is gradually emerging in the trade credit insurance market and businesses are opting for this solution in order to maintain stability. Countries like Brazil, Mexico, Chile and Argentina have higher demand for such solutions and due to increasing trade agreements and liberalization, the market in this region will see gradual upsurge. However, economic uncertainties and increasing political instability will create hurdles.

The Middle East and Africa region has witnessed the growing penetration of trade credit insurance solutions. Factors driving the demand include infrastructure development and growth in oil and gas trade in Gulf countries and export oriented policies in the countries. Increasing commercial and political risks associated with the countries in Middle East and Africa have forced many companies to take credit insurance. South Africa and UAE are important markets in the region.

Technological advancement has played an important role in the global trade credit insurance market. Usage of advanced analytics tools like artificial intelligence and big data in risk management and claims settlement is increased. New platforms help in quicker processing of policies, creditworthiness analysis and customer support. Better usage of advanced analytic techniques is predicted to enhance the risk assessment skills and operational effectiveness of the market across various regions.

The global market for trade credit insurance is expected to register significant growth because companies are trying to safeguard their financial stability and secure trade transactions. Increasing uncertainties in international trade as well as the extension of global supply chains is expected to maintain the growth of this market over a longer time period.

Top Key Players operating in the Trade Credit Insurance Market

- Allianz Trade

- Atradius N.V.

- Coface

- American International Group, Inc. (AIG)

- Zurich

- Chubb

- QBE Insurance Group Limited

- Great American Insurance Company

- Aon plc

- Credendo

- Aon plc

- EULER HERMES

- Export Development Canada

- SINOSURE

FAQ

What is trade credit insurance?

Trade credit insurance is a financial protection policy that safeguards businesses against losses caused by customer non-payment, insolvency, or delayed payments for goods and services sold on credit.

What factors are driving the growth of the trade credit insurance market?

The market is driven by increasing global trade activities, rising insolvency risks, economic uncertainties, expanding supply chains, and growing awareness among businesses regarding receivables protection.

Which region dominates the trade credit insurance market?

Europe currently dominates the market due to its strong export-oriented economies, mature insurance sector, and widespread adoption of credit risk management practices.

How does trade credit insurance benefit businesses?

Trade credit insurance helps businesses improve cash flow stability, reduce bad debt losses, support international expansion, enhance borrowing capacity, and strengthen overall financial risk management.